Discover some of the subtleties in 401(k) pricing as some fees can impact the growth of your account. Learn what you need to know to manage your retirement savings.

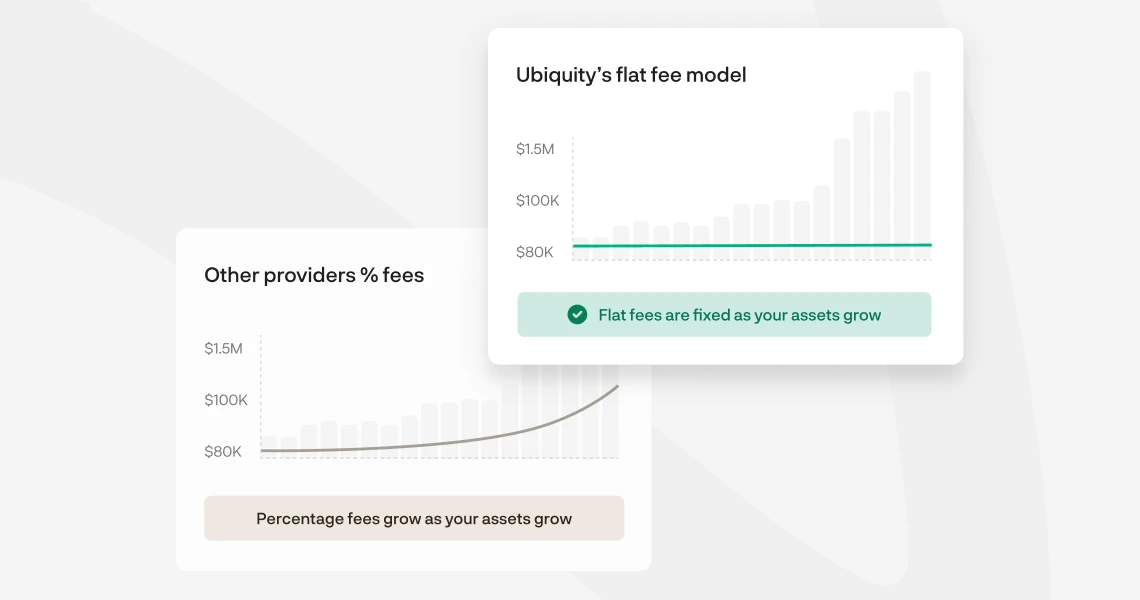

Flat-fee 401(k) plans charge a fixed cost regardless of account balance, providing predictable expenses and protecting savings as plan assets grow over time.

AUM (asset under management) fees are charged as a percentage of total plan assets, meaning costs increase as the plan grows and can significantly reduce long-term retirement savings.

Over a 30-year horizon, the difference between a flat-fee structure and a 0.50% AUM fee can amount to tens of thousands of dollars in retained retirement savings.

Flat Fees vs. AUM Fees: Which is Best for Your Retirement Plan?

When it comes to saving for your retirement, every dollar counts. But did you know that there are different fees that can significantly impact your savings? Most small business owners don’t realize until they’ve already implemented a 401(k) that their plan either consists of a flat fee or an asset under management (AUM) cost structure and that their retirement strategy is affected.

Understanding the differences between flat fees and AUM fees now can help you make more informed decisions and keep more money in your pocket as you optimize your plan to meet your retirement goals.

What Are The Differences Between Flat Fees And AUM Fees?

Flat Fees

A flat fee structure means a fixed, single cost that doesn’t change, no matter how much is in your retirement account. This means you’re able to save more of your hard-earned money and have transparency thanks to no hidden costs. Even more, flat fees simplify managing your financial well-being as you can easily integrate consistent plan costs into your budget and truly take control of your money.

Asset Under Management (AUM) Fees

AUM fees are costs taken based on the percentage of your total assets under management. These fees can be beneficial for employers who are starting with very minimal plan assets and accounts but can increase as your business and assets grow. This means depending on your growth, a plan with an AUM structure can be more expensive to manage and require more maintenance.

Which Fee Type Should You Choose?

For solopreneurs and small business owners who are looking for long-term savings, clarity, and easy manageability, choosing a retirement plan with flat fees would be best. AUM fees can quickly spiral and reduce the value of your portfolio before you even realize it. Because cost structure depends on the type of 401(k) you get and your plan provider, and you will want to do your research beforehand to ensure your best-fit plan has the right pricing for your needs.

Flat Fees Vs. AUM Fees In Action

To see the impact of flat fees over AUM fees, consider the example below of Jennifer and Joshua. Both start with 401(k)s valued at $50,000. Jennifer’s plan with Ubiquity Retirement + Savings incurs a flat fee of $6/month with an investment expense fee of 0.17%. Joshua’s plan is percentage-based, charging 0.50% annually along with an investment expense fee of 0.17%. Assuming no further contributions and an average annual growth of 10%, after 30 years:

Jennifer’s account: $823,470 with total fees of $14,142

Joshua’s account: $714,132 with total fees of $50,217

What’s the difference? Ubiquity’s flat fees could mean potentially saving $109,338 over 30 years when compared to percentage-based fees.

How Ubiquity Can Help Boost Your Retirement Future

At Ubiquity, our transparent, flat fee cost structure gives you flexibility and innovative plan features at a predictable cost. With no hidden fees, you can grow your assets confidently and never worry about rising costs as your balance grows. See how we compare with the best small business 401(k) providers or learn how to open a small business 401(k) for your team. Ready to get started? Book a complimentary meeting with our experts.

recommended resource

Ubiquity’s Guide to Small Business 401(k) Plans

Tailored for small businesses, this guide helps take the complexities out of retirement planning with actionable tips and strategies, and future-thinking insights.

Flat Fees vs. AUM Fees: Which is Best for Your Retirement Plan?

When it comes to saving for your retirement, every dollar counts. But did you know that there are different fees that can significantly impact your savings? Most small business owners don’t realize until they’ve already implemented a 401(k) that their plan either consists of a flat fee or an asset under management (AUM) cost structure and that their retirement strategy is affected.

Understanding the differences between flat fees and AUM fees now can help you make more informed decisions and keep more money in your pocket as you optimize your plan to meet your retirement goals.

What Are The Differences Between Flat Fees And AUM Fees?

Flat Fees

A flat fee structure means a fixed, single cost that doesn’t change, no matter how much is in your retirement account. This means you’re able to save more of your hard-earned money and have transparency thanks to no hidden costs. Even more, flat fees simplify managing your financial well-being as you can easily integrate consistent plan costs into your budget and truly take control of your money.

Asset Under Management (AUM) Fees

AUM fees are costs taken based on the percentage of your total assets under management. These fees can be beneficial for employers who are starting with very minimal plan assets and accounts but can increase as your business and assets grow. This means depending on your growth, a plan with an AUM structure can be more expensive to manage and require more maintenance.

Which Fee Type Should You Choose?

For solopreneurs and small business owners who are looking for long-term savings, clarity, and easy manageability, choosing a retirement plan with flat fees would be best. AUM fees can quickly spiral and reduce the value of your portfolio before you even realize it. Because cost structure depends on the type of 401(k) you get and your plan provider, and you will want to do your research beforehand to ensure your best-fit plan has the right pricing for your needs.

Flat Fees Vs. AUM Fees In Action

To see the impact of flat fees over AUM fees, consider the example below of Jennifer and Joshua. Both start with 401(k)s valued at $50,000. Jennifer’s plan with Ubiquity Retirement + Savings incurs a flat fee of $6/month with an investment expense fee of 0.17%. Joshua’s plan is percentage-based, charging 0.50% annually along with an investment expense fee of 0.17%. Assuming no further contributions and an average annual growth of 10%, after 30 years:

Jennifer’s account: $823,470 with total fees of $14,142

Joshua’s account: $714,132 with total fees of $50,217

What’s the difference? Ubiquity’s flat fees could mean potentially saving $109,338 over 30 years when compared to percentage-based fees.

How Ubiquity Can Help Boost Your Retirement Future

At Ubiquity, our transparent, flat fee cost structure gives you flexibility and innovative plan features at a predictable cost. With no hidden fees, you can grow your assets confidently and never worry about rising costs as your balance grows. See how we compare with the best small business 401(k) providers or learn how to open a small business 401(k) for your team. Ready to get started? Book a complimentary meeting with our experts.

Watch on-demand

Enter a few of your details below to view the webinar

Thank you!

Your submission has been received! Now you can watch the webinar on-demand by clicking the button below.

Flat Fees vs. AUM Fees: Which is Best for Your Retirement Plan?

When it comes to saving for your retirement, every dollar counts. But did you know that there are different fees that can significantly impact your savings? Most small business owners don’t realize until they’ve already implemented a 401(k) that their plan either consists of a flat fee or an asset under management (AUM) cost structure and that their retirement strategy is affected.

Understanding the differences between flat fees and AUM fees now can help you make more informed decisions and keep more money in your pocket as you optimize your plan to meet your retirement goals.

What Are The Differences Between Flat Fees And AUM Fees?

Flat Fees

A flat fee structure means a fixed, single cost that doesn’t change, no matter how much is in your retirement account. This means you’re able to save more of your hard-earned money and have transparency thanks to no hidden costs. Even more, flat fees simplify managing your financial well-being as you can easily integrate consistent plan costs into your budget and truly take control of your money.

Asset Under Management (AUM) Fees

AUM fees are costs taken based on the percentage of your total assets under management. These fees can be beneficial for employers who are starting with very minimal plan assets and accounts but can increase as your business and assets grow. This means depending on your growth, a plan with an AUM structure can be more expensive to manage and require more maintenance.

Which Fee Type Should You Choose?

For solopreneurs and small business owners who are looking for long-term savings, clarity, and easy manageability, choosing a retirement plan with flat fees would be best. AUM fees can quickly spiral and reduce the value of your portfolio before you even realize it. Because cost structure depends on the type of 401(k) you get and your plan provider, and you will want to do your research beforehand to ensure your best-fit plan has the right pricing for your needs.

Flat Fees Vs. AUM Fees In Action

To see the impact of flat fees over AUM fees, consider the example below of Jennifer and Joshua. Both start with 401(k)s valued at $50,000. Jennifer’s plan with Ubiquity Retirement + Savings incurs a flat fee of $6/month with an investment expense fee of 0.17%. Joshua’s plan is percentage-based, charging 0.50% annually along with an investment expense fee of 0.17%. Assuming no further contributions and an average annual growth of 10%, after 30 years:

Jennifer’s account: $823,470 with total fees of $14,142

Joshua’s account: $714,132 with total fees of $50,217

What’s the difference? Ubiquity’s flat fees could mean potentially saving $109,338 over 30 years when compared to percentage-based fees.

How Ubiquity Can Help Boost Your Retirement Future

At Ubiquity, our transparent, flat fee cost structure gives you flexibility and innovative plan features at a predictable cost. With no hidden fees, you can grow your assets confidently and never worry about rising costs as your balance grows. See how we compare with the best small business 401(k) providers or learn how to open a small business 401(k) for your team. Ready to get started? Book a complimentary meeting with our experts.

Get your guide

Enter your details below to download your free PDF now

Thank you!

Your submission has been received! Now you can download the guide by clicking the button below.

Let’s connect and talk about how Ubiquity can support your efforts.

401k Pricing Flat Fees vs Percentage Fees

Discover some of the subtleties in 401(k) pricing as some fees can impact the growth of your account. Learn what you need to know to manage your retirement savings.