What is Delaware EARNS?

The Delaware EARNS program is a state-administered retirement program aimed to help employees start saving for the future they want. Historically, saving for retirement hasn’t been as accessible, especially for smaller businesses that may not have the resources to offer a plan on their own. That’s where Delaware EARNS comes in as a simple, affordable option that businesses can utilize. Besides the state-run program, employers can also choose to go with a private option, like a 401(k), 403(b), or even a Safe Harbor plan, all of which offer different levels of flexibility, cost-efficiency, and benefits than Delaware EARNS (and might actually be more profitable in the long run, depending on your business).

Below, we dive into everything you need to know about Delaware EARNS so you can make the best choice for your business and employees.

Key Deadlines and Time Frame

Delaware EARNS officially launched in late 2024, and employers had until October 15, 2024 to register their businesses and certify exemptions. According to the program’s site, newly eligible businesses had a deadline of June 30, 2025. If you have been previously notified about registration and haven’t made a move yet to move forward with the state-run option or a private plan, it’s crucial to make a decision soon before any consequences happen.

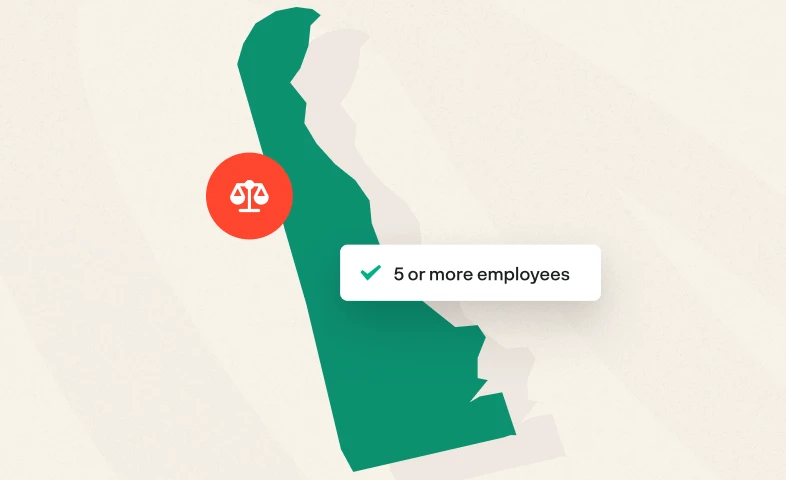

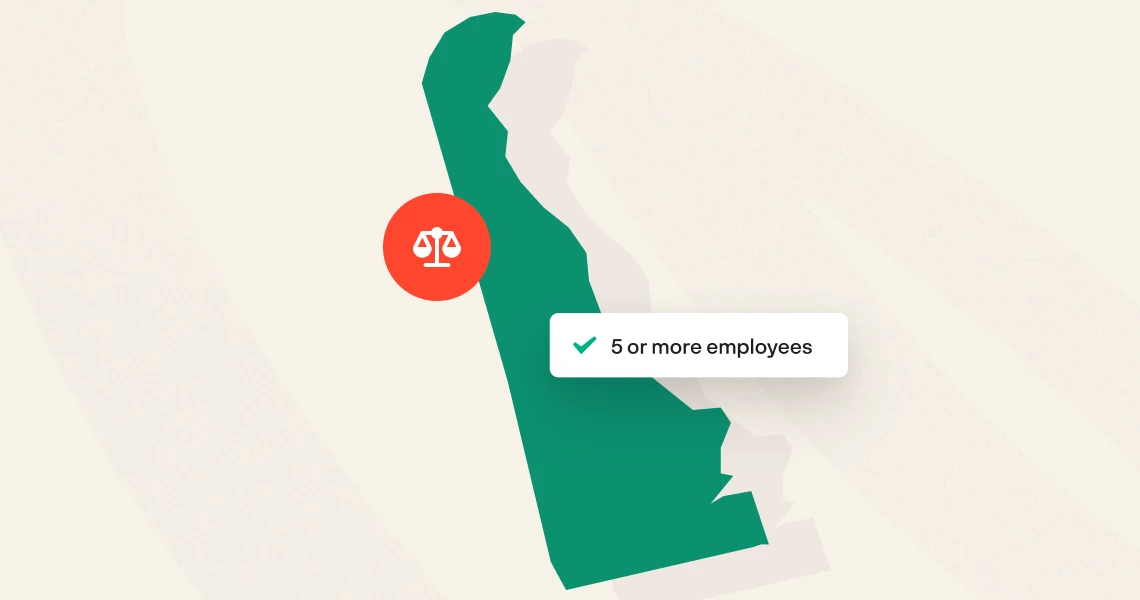

Who is Required to Participate in the Delaware EARNS Program?

If your business meets the following criteria, you’ll be required to participate in the state-run program:

- Have five or more employees

- Don’t already offer a qualified retirement plan (401(k), 403(b), etc.)

- Have been in business for at least 12 months

Don’t forget: If you already have a retirement plan, you’re still not automatically exempt! You’ll have to certify your exemption through the Delaware EARNS portal.

Attributes and Directives Employers Need to Know

Compliance Options

It’s important to remember that participation in any kind of retirement plan isn’t just to check a box–it’s to stay compliant with Delaware and IRS requirements. Besides staying compliant by participating in Delaware EARNS, employers can choose a private plan, like a 401(k), if they don’t want to be held back by state-run limitations.

Employer Responsibilities

Employers are simply facilitators of the state-run program, but they also have various responsibilities including:

- Registering for the program by the state’s deadline

- Providing employee information for enrollment

- Setting up payroll deductions

- Staying up to date with program needs

Costs & Fees

While employers won’t be charged any direct fees to take part in Delaware EARNS, employees will have to pay administrative fees, which are taken out of their investment returns. The exact amount depends on the plan’s structure. Unsurprisingly, this can be a deal breaker because if employees are impacted financially, their employers will be also in different ways. This factor alone is a significant reason why many employers explore private plans, especially those with more cost-effective models like flat fees.

Employee Experience

Once they’re enrolled, employees can choose between different investment options, save automatically through payroll deductions, and opt out or change their contribution rates at any time. Additionally, their account is portable, so they can take it from job to job.

Are there Penalties for Noncompliance?

Yes, employers who do not register or fail to comply with program requirements will face penalties. Initially, the state will send a notice to employers about their noncompliance, giving them a chance to fix the issue within 90 days. If they don’t, they may have to pay fines of up to $250 per employee per year, with a maximum penalty of $5,000 per year. So, get registered or claim exemption early, and ensure you follow all the requirements so you don’t have to give your hard-earned money away!

What Other Plan Options Can I Utilize?

As mentioned earlier, if you don’t have to go with the Delaware EARNS program, you can choose a private run retirement plan instead. Some popular options include:

- Traditional 401(k) Plans: Known as the most robust and flexible option, a 401(k) offers extensive benefits with everything from contribution limits to plan design and administration. Bonus: You may be able to qualify for tax credits to offset the costs of setup and maintenance.

- Safe Harbor 401(k): Think of this one as very similar to a 401(k), but with a few more requirements so you can avoid yearly IRS nondiscrimination testing. This is especially attractive for employers who are looking to avoid the complexities of compliance while maximizing their own contributions.

- SIMPLE IRA: This option is even simpler than a 401(k), but there’s a tradeoff: You’ll get less customization options and fewer investment choices. This is ideal for a business that wants to just start with the most basic plan possible before converting into something else, like a 401(k).

What Do Employers Need to Do Now to Prepare for and Participate in the Delaware EARNS Program?

Here’s how employers can get ready in five steps:

- Check your eligibility: Your registration depends on employee count and amount of time you’ve been in business, so make sure to confirm everything.

- Stay up to date on updates: Keep up with legislative changes, especially if you have a newer business and the original October 2024 deadline didn’t apply to you.

- Evaluate other options: Don’t skip out on exploring private plans. You might find that another type of plan like a 401(k) or SIMPLE IRA provides more cost-efficiency and flexibility for your business goals.

- Talk to a plan provider: Whether you choose the state-run option or a private plan, talking to a provider now is valuable as they can provide unbiased guidance and help you better understand the best move for your business.

- Educate your team: You’ll have to communicate updates with your employees and ensure they have the resources they need to make the most out of their retirement plan.

Conclusion

Even though the Delaware EARNS deadline has already passed for eligible businesses, it’s not too late to get on track by registering for the program and going with a private plan. The important thing is to make a decision, implement a plan, and start strategizing for employees’ (and your company’s) futures.

If you still need help figuring out the right plan for your business, Ubiquity is here to help. We offer flat-fee, customizable 401(k) solutions that are designed for optimal scalability and profitability. While providing benefits like higher contributions and more investment options for your employees, you can also benefit from tax credits, hands-off administration, and much more.