Ubiquity’s Mega Roth option in Single(k) lets business owners optimize savings with additional after-tax contributions, beyond what's possible in a 401(k) plan.

A Mega Backdoor Roth is a retirement savings strategy that allows eligible, high-earning savers to move additional after-tax 401(k) contributions into a Roth account for more tax-free growth.

This strategy may help business owners and employees build additional tax diversification and long-term retirement flexibility by increasing savings potential.

Not all 401(k) plans support Mega Backdoor Roth contributions, as plans must allow after-tax contributions and Roth conversions.

For high earners looking to save more for retirement, traditional contribution limits can sometimes feel restrictive. Even after maxing out a 401(k) or IRA, many business owners and employees still want additional ways to build long-term, tax-advantaged retirement income. That’s where the Mega Backdoor Roth strategy comes in.

A Mega Backdoor Roth allows eligible retirement savers to contribute more of their after-tax dollars into their Roth account, meaning bigger tax-free growth and withdrawals later in retirement. And with 2026 contribution limits having changed, this strategy is gaining even more attention among earners who want greater retirement planning flexibility.

In this guide, we’ll break down how a Mega Backdoor Roth works, who qualifies, current contribution limits, potential tax considerations, and more.

What is a Mega Backdoor Roth?

As mentioned, a Mega Backdoor Roth is a special retirement plan strategy that allows high-earning employees to save more by contributing additional after-tax dollars into their Roth account. Unlike a traditional Roth IRA, which has income restrictions and lower annual contribution limits, a Mega Backdoor Roth uses a higher overall 401(k) contribution limit to potentially allow significantly larger Roth contributions.

While more employees are using a Mega Backdoor Roth, not all of them have access to this strategy because not all 401(k) plans support it. To be able to use it, plans must generally allow:

After-tax 401(k) contributions

In-service Roth contributions

How Does a Mega Backdoor Roth Work?

Here’s a simplified version of how this strategy works:

An employee contributes the standard 401(k) maximum

Their employer contributes matching or profit-sharing contributions

If the plan allows, the employee may contribute additional after-tax dollars to the overall maximum 401(k) contribution limit

Those after-tax contributions can then be converted into a Roth 401(k) or Roth IRA

Again, it’s important to remember that not every 401(k) plan offers the Mega Backdoor Roth flexibility, which is why many employers often choose providers that are able to support customizable plan features and advanced retirement savings strategies.

Who Qualifies for a Mega Backdoor Roth?

There really aren’t restrictions on who is able to participate in a Mega Backdoor Roth strategy. As long as a business owner has a plan that supports it, than employees are able to take part in it. But, there may be some people who benefit from the strategy more, including:

High-income earners who are already maxing out traditional 401(k) contributions

Business owners looking to increase tax-advantaged retirement savings

Employees who want additional Roth savings opportunities

Savers who are focused on long-term tax diversification

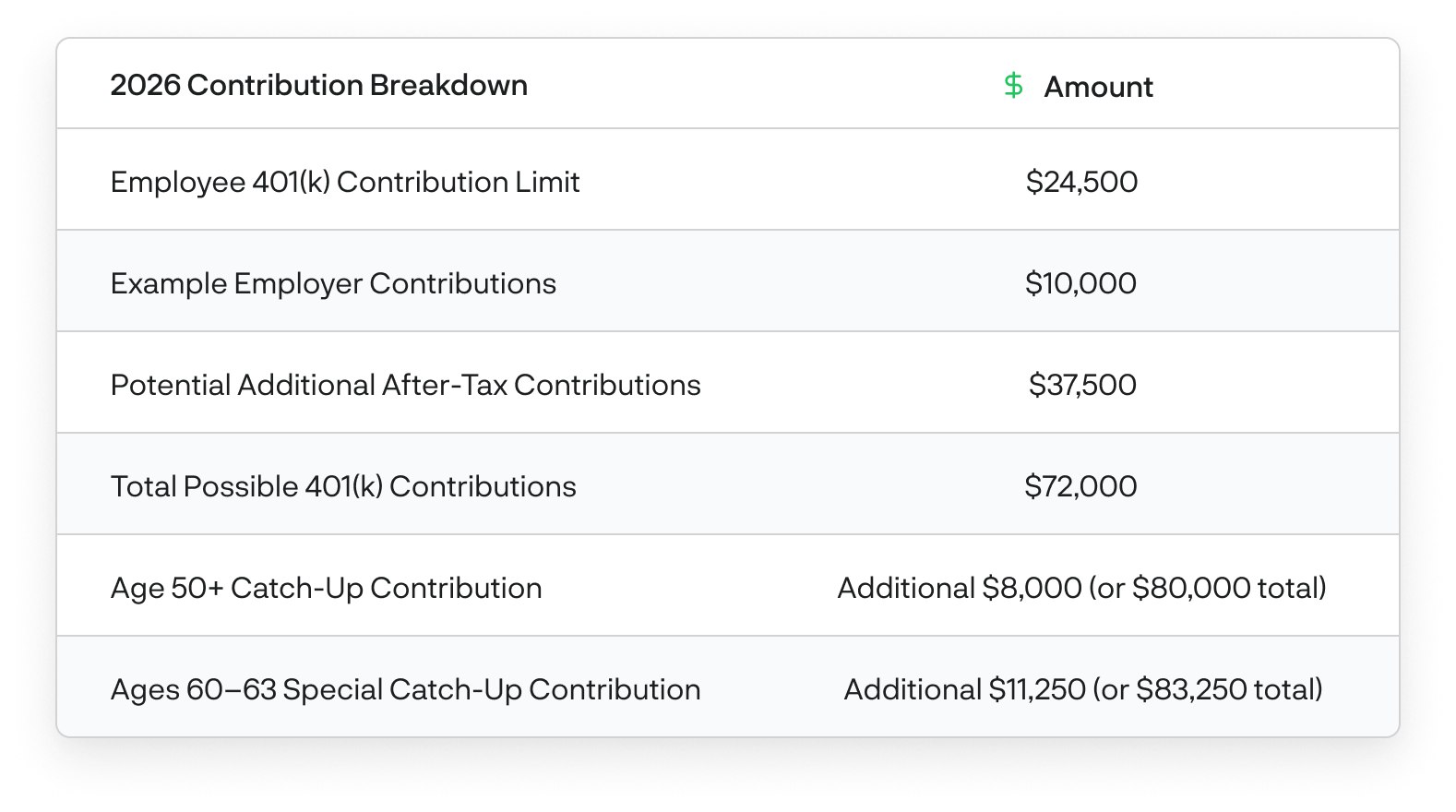

Mega Backdoor Roth Contribution Limits for 2026

Mega Backdoor Roth contribution limits are based on the IRS annual 401(k) contribution maximums.

What are the Benefits of a Mega Backdoor Roth?

Some potential benefits include:

Increased Roth savings potential - A traditional Roth account does have limitations, especially for earners who hit a certain income threshold. A Mega Backdoor Roth allows these earners to go around the rules a bit legally and contribute significantly more than what the usual rules normally allow.

Potential for tax-free growth - Once converted into a Roth account, qualified future withdrawals (including investment growth) may be tax-free once someone is in retirement.

No direct income limits - Mega Backdoor Roth strategies do not have direct income restrictions, meaning that there is no cap for high earners to actually participate in a qualifying plan.

Enhanced benefits for business owners - Offering Mega Backdoor Roth contributions may help with attracting and retaining employees who are focused on long-term financial planning and standing out more in competitive markets overall.

What are the Potential Drawbacks and Considerations?

Despite the significant savings opportunities, a Mega Backdoor Roth strategy still has several important considerations to keep in mind.

Not all 401(k) plans support it - As we mentioned before, 401(k)s must generally support after-tax contributions and in-service Roth conversions to be able to have a Mega Backdoor Roth.

Additional administrative complexity - Managing after-tax contributions and Roth conversions may require additional recordkeeping, payroll coordination, and plan administration. While a provider can help alleviate some of this work, employers will still need to take care of other needs.

Potential tax implications - While after-tax contributions are not taxed again during conversion, any investment earnings generated before the conversion may still be taxable.

Contribution limits still apply - A Mega Backdoor Roth is still subject to IRS contribution limits, including employer amounts.

Plan design matters - This strategy relies heavily on plan flexibility, so employers and participants should work with a provider that can simplify 401(k) capabilities and compliance considerations.

How Ubiquity Helps Employers Build Smarter 401(k) Plans

Ultimately, Mega Backdoor Roth strategies can create valuable savings opportunities for high-income earners, business owners, and employees that are looking to take their nest eggs beyond the traditional contribution limits. But remember: because these strategies rely so heavily on plan design, it’s important to choose the right 401(k) provider upfront that can help with ongoing administration, contribution support, compliance, and more.

And at Ubiquity Retirement + Savings, we help employers get the Mega Backdoor Roth strategy they need with flexible 401(k) plans. Our plans are designed to support evolving business, and compliance goals, ensuring owners and their employees have everything they need to maximize their savings.

Frequently Asked Questions

What is a Mega Backdoor Roth?

A Mega Backdoor Roth is a retirement strategy that allows eligible participants to contribute additional after-tax dollars into a 401(k) plan and convert those funds into a Roth account. This allows for potentially more savings that go beyond traditional contribution limits.

Does a Mega Backdoor Roth have income limits?

No. Unlike direct Roth IRA contributions, Mega Backdoor Roth strategies do not have direct income limits. However, availability overall does depend on whether a 401(k) plan supports after-tax contributions and Roth conversions.

Do all 401(k) plans allow Mega Backdoor Roth contributions?

No. A 401(k) plan typically needs after-tax employee contributions and in-service Roth conversions or rollovers. Availability for a Mega Backdoor Roth will depend on your plan design and provider.

Should employers offer Mega Backdoor Roth options?

For some employers, offering Mega Backdoor Roth options can support employee financial wellness and create additional savings opportunities that encourage satisfaction and better retention. Even more, the savings can come in many ways, not just for high earners, but also business owners. So, there truly are quite a few opportunities to capitalize on for everyone involved.

recommended resource

An Employee Guide to 401(k) Plans

Here’s everything you need to know about enrolling in your company’s retirement plan.

For high earners looking to save more for retirement, traditional contribution limits can sometimes feel restrictive. Even after maxing out a 401(k) or IRA, many business owners and employees still want additional ways to build long-term, tax-advantaged retirement income. That’s where the Mega Backdoor Roth strategy comes in.

A Mega Backdoor Roth allows eligible retirement savers to contribute more of their after-tax dollars into their Roth account, meaning bigger tax-free growth and withdrawals later in retirement. And with 2026 contribution limits having changed, this strategy is gaining even more attention among earners who want greater retirement planning flexibility.

In this guide, we’ll break down how a Mega Backdoor Roth works, who qualifies, current contribution limits, potential tax considerations, and more.

What is a Mega Backdoor Roth?

As mentioned, a Mega Backdoor Roth is a special retirement plan strategy that allows high-earning employees to save more by contributing additional after-tax dollars into their Roth account. Unlike a traditional Roth IRA, which has income restrictions and lower annual contribution limits, a Mega Backdoor Roth uses a higher overall 401(k) contribution limit to potentially allow significantly larger Roth contributions.

While more employees are using a Mega Backdoor Roth, not all of them have access to this strategy because not all 401(k) plans support it. To be able to use it, plans must generally allow:

After-tax 401(k) contributions

In-service Roth contributions

How Does a Mega Backdoor Roth Work?

Here’s a simplified version of how this strategy works:

An employee contributes the standard 401(k) maximum

Their employer contributes matching or profit-sharing contributions

If the plan allows, the employee may contribute additional after-tax dollars to the overall maximum 401(k) contribution limit

Those after-tax contributions can then be converted into a Roth 401(k) or Roth IRA

Again, it’s important to remember that not every 401(k) plan offers the Mega Backdoor Roth flexibility, which is why many employers often choose providers that are able to support customizable plan features and advanced retirement savings strategies.

Who Qualifies for a Mega Backdoor Roth?

There really aren’t restrictions on who is able to participate in a Mega Backdoor Roth strategy. As long as a business owner has a plan that supports it, than employees are able to take part in it. But, there may be some people who benefit from the strategy more, including:

High-income earners who are already maxing out traditional 401(k) contributions

Business owners looking to increase tax-advantaged retirement savings

Employees who want additional Roth savings opportunities

Savers who are focused on long-term tax diversification

Mega Backdoor Roth Contribution Limits for 2026

Mega Backdoor Roth contribution limits are based on the IRS annual 401(k) contribution maximums.

What are the Benefits of a Mega Backdoor Roth?

Some potential benefits include:

Increased Roth savings potential - A traditional Roth account does have limitations, especially for earners who hit a certain income threshold. A Mega Backdoor Roth allows these earners to go around the rules a bit legally and contribute significantly more than what the usual rules normally allow.

Potential for tax-free growth - Once converted into a Roth account, qualified future withdrawals (including investment growth) may be tax-free once someone is in retirement.

No direct income limits - Mega Backdoor Roth strategies do not have direct income restrictions, meaning that there is no cap for high earners to actually participate in a qualifying plan.

Enhanced benefits for business owners - Offering Mega Backdoor Roth contributions may help with attracting and retaining employees who are focused on long-term financial planning and standing out more in competitive markets overall.

What are the Potential Drawbacks and Considerations?

Despite the significant savings opportunities, a Mega Backdoor Roth strategy still has several important considerations to keep in mind.

Not all 401(k) plans support it - As we mentioned before, 401(k)s must generally support after-tax contributions and in-service Roth conversions to be able to have a Mega Backdoor Roth.

Additional administrative complexity - Managing after-tax contributions and Roth conversions may require additional recordkeeping, payroll coordination, and plan administration. While a provider can help alleviate some of this work, employers will still need to take care of other needs.

Potential tax implications - While after-tax contributions are not taxed again during conversion, any investment earnings generated before the conversion may still be taxable.

Contribution limits still apply - A Mega Backdoor Roth is still subject to IRS contribution limits, including employer amounts.

Plan design matters - This strategy relies heavily on plan flexibility, so employers and participants should work with a provider that can simplify 401(k) capabilities and compliance considerations.

How Ubiquity Helps Employers Build Smarter 401(k) Plans

Ultimately, Mega Backdoor Roth strategies can create valuable savings opportunities for high-income earners, business owners, and employees that are looking to take their nest eggs beyond the traditional contribution limits. But remember: because these strategies rely so heavily on plan design, it’s important to choose the right 401(k) provider upfront that can help with ongoing administration, contribution support, compliance, and more.

And at Ubiquity Retirement + Savings, we help employers get the Mega Backdoor Roth strategy they need with flexible 401(k) plans. Our plans are designed to support evolving business, and compliance goals, ensuring owners and their employees have everything they need to maximize their savings.

Frequently Asked Questions

What is a Mega Backdoor Roth?

A Mega Backdoor Roth is a retirement strategy that allows eligible participants to contribute additional after-tax dollars into a 401(k) plan and convert those funds into a Roth account. This allows for potentially more savings that go beyond traditional contribution limits.

Does a Mega Backdoor Roth have income limits?

No. Unlike direct Roth IRA contributions, Mega Backdoor Roth strategies do not have direct income limits. However, availability overall does depend on whether a 401(k) plan supports after-tax contributions and Roth conversions.

Do all 401(k) plans allow Mega Backdoor Roth contributions?

No. A 401(k) plan typically needs after-tax employee contributions and in-service Roth conversions or rollovers. Availability for a Mega Backdoor Roth will depend on your plan design and provider.

Should employers offer Mega Backdoor Roth options?

For some employers, offering Mega Backdoor Roth options can support employee financial wellness and create additional savings opportunities that encourage satisfaction and better retention. Even more, the savings can come in many ways, not just for high earners, but also business owners. So, there truly are quite a few opportunities to capitalize on for everyone involved.

Watch on-demand

Enter a few of your details below to view the webinar

Thank you!

Your submission has been received! Now you can watch the webinar on-demand by clicking the button below.

For high earners looking to save more for retirement, traditional contribution limits can sometimes feel restrictive. Even after maxing out a 401(k) or IRA, many business owners and employees still want additional ways to build long-term, tax-advantaged retirement income. That’s where the Mega Backdoor Roth strategy comes in.

A Mega Backdoor Roth allows eligible retirement savers to contribute more of their after-tax dollars into their Roth account, meaning bigger tax-free growth and withdrawals later in retirement. And with 2026 contribution limits having changed, this strategy is gaining even more attention among earners who want greater retirement planning flexibility.

In this guide, we’ll break down how a Mega Backdoor Roth works, who qualifies, current contribution limits, potential tax considerations, and more.

What is a Mega Backdoor Roth?

As mentioned, a Mega Backdoor Roth is a special retirement plan strategy that allows high-earning employees to save more by contributing additional after-tax dollars into their Roth account. Unlike a traditional Roth IRA, which has income restrictions and lower annual contribution limits, a Mega Backdoor Roth uses a higher overall 401(k) contribution limit to potentially allow significantly larger Roth contributions.

While more employees are using a Mega Backdoor Roth, not all of them have access to this strategy because not all 401(k) plans support it. To be able to use it, plans must generally allow:

After-tax 401(k) contributions

In-service Roth contributions

How Does a Mega Backdoor Roth Work?

Here’s a simplified version of how this strategy works:

An employee contributes the standard 401(k) maximum

Their employer contributes matching or profit-sharing contributions

If the plan allows, the employee may contribute additional after-tax dollars to the overall maximum 401(k) contribution limit

Those after-tax contributions can then be converted into a Roth 401(k) or Roth IRA

Again, it’s important to remember that not every 401(k) plan offers the Mega Backdoor Roth flexibility, which is why many employers often choose providers that are able to support customizable plan features and advanced retirement savings strategies.

Who Qualifies for a Mega Backdoor Roth?

There really aren’t restrictions on who is able to participate in a Mega Backdoor Roth strategy. As long as a business owner has a plan that supports it, than employees are able to take part in it. But, there may be some people who benefit from the strategy more, including:

High-income earners who are already maxing out traditional 401(k) contributions

Business owners looking to increase tax-advantaged retirement savings

Employees who want additional Roth savings opportunities

Savers who are focused on long-term tax diversification

Mega Backdoor Roth Contribution Limits for 2026

Mega Backdoor Roth contribution limits are based on the IRS annual 401(k) contribution maximums.

What are the Benefits of a Mega Backdoor Roth?

Some potential benefits include:

Increased Roth savings potential - A traditional Roth account does have limitations, especially for earners who hit a certain income threshold. A Mega Backdoor Roth allows these earners to go around the rules a bit legally and contribute significantly more than what the usual rules normally allow.

Potential for tax-free growth - Once converted into a Roth account, qualified future withdrawals (including investment growth) may be tax-free once someone is in retirement.

No direct income limits - Mega Backdoor Roth strategies do not have direct income restrictions, meaning that there is no cap for high earners to actually participate in a qualifying plan.

Enhanced benefits for business owners - Offering Mega Backdoor Roth contributions may help with attracting and retaining employees who are focused on long-term financial planning and standing out more in competitive markets overall.

What are the Potential Drawbacks and Considerations?

Despite the significant savings opportunities, a Mega Backdoor Roth strategy still has several important considerations to keep in mind.

Not all 401(k) plans support it - As we mentioned before, 401(k)s must generally support after-tax contributions and in-service Roth conversions to be able to have a Mega Backdoor Roth.

Additional administrative complexity - Managing after-tax contributions and Roth conversions may require additional recordkeeping, payroll coordination, and plan administration. While a provider can help alleviate some of this work, employers will still need to take care of other needs.

Potential tax implications - While after-tax contributions are not taxed again during conversion, any investment earnings generated before the conversion may still be taxable.

Contribution limits still apply - A Mega Backdoor Roth is still subject to IRS contribution limits, including employer amounts.

Plan design matters - This strategy relies heavily on plan flexibility, so employers and participants should work with a provider that can simplify 401(k) capabilities and compliance considerations.

How Ubiquity Helps Employers Build Smarter 401(k) Plans

Ultimately, Mega Backdoor Roth strategies can create valuable savings opportunities for high-income earners, business owners, and employees that are looking to take their nest eggs beyond the traditional contribution limits. But remember: because these strategies rely so heavily on plan design, it’s important to choose the right 401(k) provider upfront that can help with ongoing administration, contribution support, compliance, and more.

And at Ubiquity Retirement + Savings, we help employers get the Mega Backdoor Roth strategy they need with flexible 401(k) plans. Our plans are designed to support evolving business, and compliance goals, ensuring owners and their employees have everything they need to maximize their savings.

Frequently Asked Questions

What is a Mega Backdoor Roth?

A Mega Backdoor Roth is a retirement strategy that allows eligible participants to contribute additional after-tax dollars into a 401(k) plan and convert those funds into a Roth account. This allows for potentially more savings that go beyond traditional contribution limits.

Does a Mega Backdoor Roth have income limits?

No. Unlike direct Roth IRA contributions, Mega Backdoor Roth strategies do not have direct income limits. However, availability overall does depend on whether a 401(k) plan supports after-tax contributions and Roth conversions.

Do all 401(k) plans allow Mega Backdoor Roth contributions?

No. A 401(k) plan typically needs after-tax employee contributions and in-service Roth conversions or rollovers. Availability for a Mega Backdoor Roth will depend on your plan design and provider.

Should employers offer Mega Backdoor Roth options?

For some employers, offering Mega Backdoor Roth options can support employee financial wellness and create additional savings opportunities that encourage satisfaction and better retention. Even more, the savings can come in many ways, not just for high earners, but also business owners. So, there truly are quite a few opportunities to capitalize on for everyone involved.

Get your guide

Enter your details below to download your free PDF now

Thank you!

Your submission has been received! Now you can download the guide by clicking the button below.

Let’s connect and talk about how Ubiquity can support your efforts.

Mega Backdoor Roth Explained: How This Strategy Helps High Earners Save More

Ubiquity’s Mega Roth option in Single(k) lets business owners optimize savings with additional after-tax contributions, beyond what's possible in a 401(k) plan.