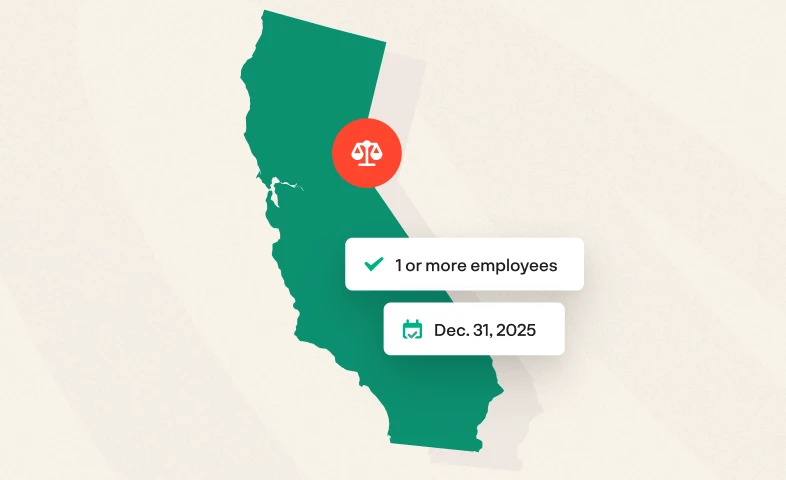

CalSavers Explained: Timeline, Requirements, & Specifications

Everyone

Employers & Business Owners

RetirePath VA Explained: Timeline, Requirements, & Specifications

Everyone

Employers & Business Owners

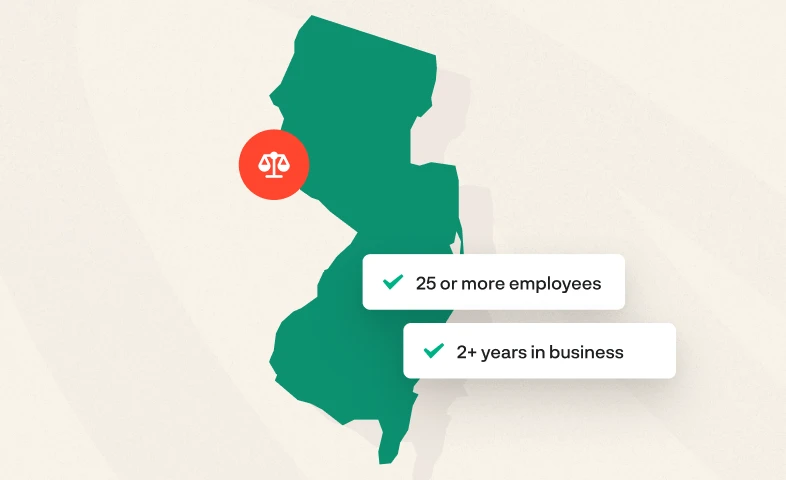

RetireReady NJ Explained: Timeline, Requirements, & Specifications

Everyone

Employers & Business Owners

401(k) vs. State-Mandated Plans: Understanding What's Right for Your Business

Everyone

Employers & Business Owners

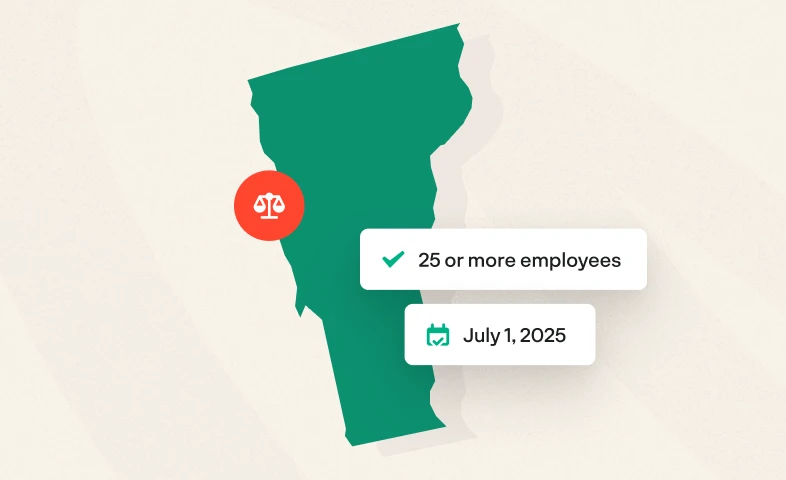

Vermont Saves Explained: Timeline, Requirements, & Specifications

Everyone

Employers & Business Owners

Generation X Has All Eyes on Preparing for Retirement

Everyone

Outpacing Inflation: Modern Retirement Strategies for Small Business & Gig Workers

Everyone

Employers & Business Owners

2025 Playbook for Small Business Employee Benefits: Why 401(k)s Are a Must

Everyone

Employees

The Small Business Owner’s Guide to State-Mandated Retirement Plans

Everyone

Employers & Business Owners

401(k) Loans: Rules & What to Know in 2025

Everyone

Employees

How Much Do Companies Typically Match on 401(k)

Everyone

Employees

The Complete Solo 401(k) Starter Guide

Everyone

Employers & Business Owners

%20costs%20and%20savings.webp)