What is the Minnesota Secure Choice Retirement Program?

The Minnesota Secure Choice program aims to close the retirement gap by targeting business owners across all industries and requiring them to register in the program or implement a qualified private plan. The program helps employees save more with automatic payroll deductions that get put into an IRA, which is managed through the Minnesota State Board of Investment. If you’re a business owner and don’t currently offer a retirement plan, you’ll want your next steps to be all about learning more about Secure Choice, how you can get started, and how a private can be the better fit for your business compared to a state-run option–all of which we’ll help with below.

Key Deadlines and Timeframe

According to the Secure Choice website, the program is expected to go into full swing starting in early January 2026. Once it launches, employers will be given specified times to get registered. For example, those with 100 or more employees will be phased into the program within the first six months after launch, and those with 50-99 employees will be expected to follow soon after.

Who is Required to Participate in the Minnesota Secure Choice Program?

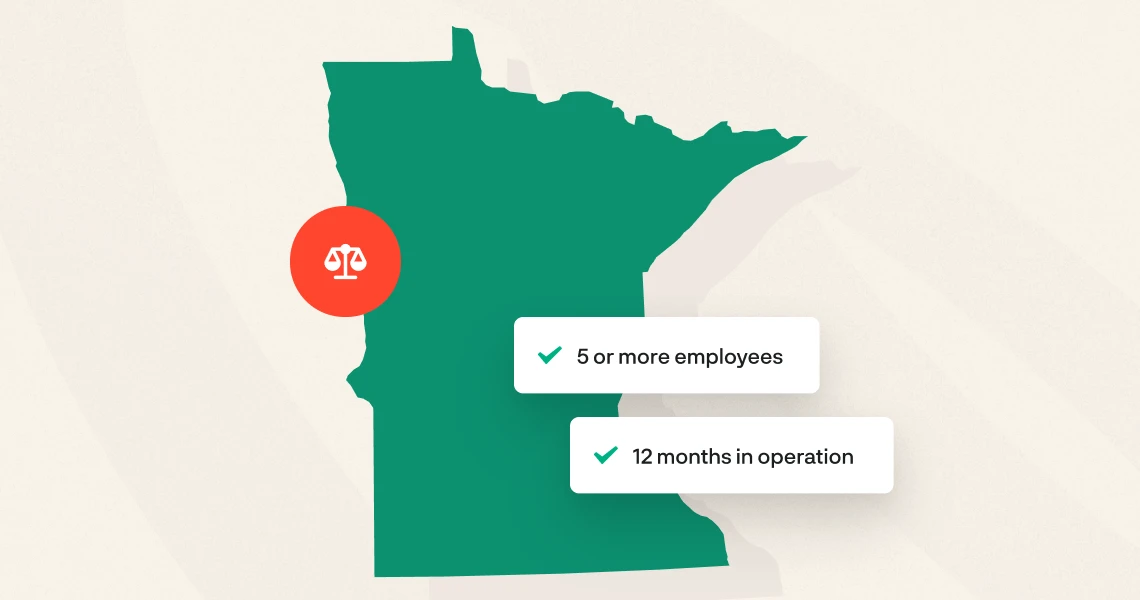

Regardless of industry, registration for Secure Choice is mandatory if you’re an employer that:

- Has five or more employees

- Have been in business for at least 12 months

- Do not currently offer a qualified retirement plan (401(k), SIMPLE IRA, etc.)

If you already have an established retirement plan, you’ll have to claim exemption through the Secure Choice platform. You’re not exempted automatically!

Attributes and Directives Employers Need to Know

Automatic Enrollment

Eligible employees are automatically enrolled into the program at a default contribution rate, ensuring that they can take advantage of the benefits from day one. They can opt-out or change the rate at any time.

Individual Retirement Accounts (IRAs)

Roth IRAs are used by default for contributions, but employees may switch to a traditional IRA if they want to. Their accounts will follow them from job to job.

Employee Contributions Only

Employers are not required to contribute to employees’ accounts–you’ll only need to focus on administration, managing deductions, and ensuring information is provided when necessary. This setup may not be ideal for every business as you can miss out on significant opportunities to attract and retain talent, or stand out in a competitive market.

Investment Management (by the Minnesota State Board of Investment)

The state oversees all investment options, which has its pros and cons for employers. This might be fine to start but in the long-term, employees may seek out a broader fund lineup so they can better tailor their accounts to their goals. Broader investment options are available with plans like 401(k)s, etc.

Employer Registration & Enrollment

Employers won’t have to guess when it’s time for them to register. The state will let you know when it’s your turn, and provide you with the steps to confirm eligibility, upload employee information, and set up payroll deductions.

Payroll Deductions & Contributions

Employers are responsible for processing deductions and submitting contributions each pay period. The state will provide you the tools to do this as efficiently as possible.

Employee Education

Minnesota will provide ongoing educational resources to help employees understand how the program works and how to manage their accounts.

Are there Penalties for Noncompliance?

Although specific fines and penalties are still being finalized, it’s highly likely that employers that aren’t registered or exempt will face consequences soon. Penalties can be established at any time, so if you haven’t enrolled yet or explored how to navigate the program’s processes, it’s important to do so soon as this will save you time and unnecessary costs!

What are Other Plan Choices to Choose From?

If you find that the Secure Choice program isn’t the perfect fit for your business, you’ll want to choose a private retirement plan instead. In many cases, these plans offer more flexibility, affordability, simplicity, and more added value than state-run plans. Here are some alternatives to consider:

401(k) Plans

A traditional 401(k) is the highly customizable option that allows for both employer and employee contributions without excessive costs, complexity, or hands-on management. With features like higher contribution limits, tax advantages, and broad investment options, you can keep your business profitable while supporting your employees’ futures.

Safe Harbor Plans

Think of a version as a simplified version of a 401(k). These plans are designed for employers to automatically pass the yearly IRS nondiscrimination tests as long as they follow certain requirements. They’re ideal for owners who want to avoid complex compliance requirements, reduce taxable income, and enhance the saving potential of themselves and their employees.

SIMPLE IRA

A lower-cost alternative to a 401(k), SIMPLE IRAs are known for being easy to set up and manage. But the simplicity doesn’t come without sacrifices: SIMPLE IRAs have lower contribution limits and mandatory employer contributions, which may not be ideal if you want full flexibility.

What Do Employers Need to Do Now to Prepare for and Participate in the Minnesota Secure Choice Retirement Program?

Here are five things to keep in mind as you prepare for the program’s deadlines:

- Stay up to date on changes: Regularly check out updates from the Secure Choice site, or from Ubiquity’s state legislation page.

- Check your exemption: If you already offer a retirement plan, gather your documents so you can prove you’re exempt when it’s time.

- Explore other plan options: Be sure to explore other providers and learn how plans like a 401(k) may be a better fit for your business’ needs.

- Talk to your payroll provider: Ensure they know about your upcoming changes, whether you go with Secure Choice or a private plan, so they can assist with integration.

- Educate your team: Use available resources and tools to educate your team on what’s ahead.

Conclusion

Even though deadlines are still a while away, now is the right time to prepare your retirement strategy. Whether you choose to participate in the Secure Choice program or opt in for a 401(k) or another type of private plan, making a decision on what to offer as soon as possible will help you better support your employees while driving you to reach your business goals.

At Ubiquity, we offer 401(k) solutions that are low-maintenance, high-reward alternatives to state-run plans. With a flat-fee model and customizable plan designs, you can get the flexibility and affordability you need to scale your company with ease and set your business apart from the competition.