Safe Harbor 401(k) plans help employers avoid certain yearly nondiscrimination requirements.

To take advantage of this type of plan’s benefits, employers must make qualifying contributions to employees through matching or nonelective contributions.

SECURE 2.0 introduced additional opportunities and considerations for Safe Harbor plan design.

Safe Harbor 401(k) plans have become one of the most popular retirement plan options for growing businesses, especially for owners who are looking to simplify compliance, maximize retirement contributions, and offer competitive employee benefits.

Below, you can expect to learn:

what a Safe Harbor 401(k) is

how Safe Harbor contributions work

the different Safe Harbor plan types

compliance and testing considerations

deadlines and rules employers should know

What is a Safe Harbor 401(k):

Safe Harbor 401(k) plans are designed to encourage more employee participation while helping employers satisfy specific IRS compliance requirements without extra work, especially when it comes to highly compensated employees.

With a traditional 401(k), annual nondiscrimination testing measures whether retirement benefits are fairly proportioned between highly compensated and non-highly compensated employees. If a plan fails testing, employers may need to:

issue corrective refunds

make additional employer contributions

adjust plan administration

A Safe Harbor plan reduces this risk by requiring employers to make approved contributions on behalf of employees. As long as employers follow a Safe Harbor’s rules, they can benefit from:

At first look, a Safe Harbor 401(k) can seem like a traditional plan. Employees contribute to a Safe Harbor through payroll deferral, like they would with a traditional 401(k). But the difference is that employers are required to make qualifying contributions on behalf of eligible employees using an approved Safe Harbor formula, which a plan provider can help create.

There are a few requirements to these contributions, including that they may be:

matching contributions tied to employee deferrals

nonelective contributions made regardless of participation

In return, employers can avoid certain annual testing requirements that they wouldn’t be able to get out of with a traditional 401(k).

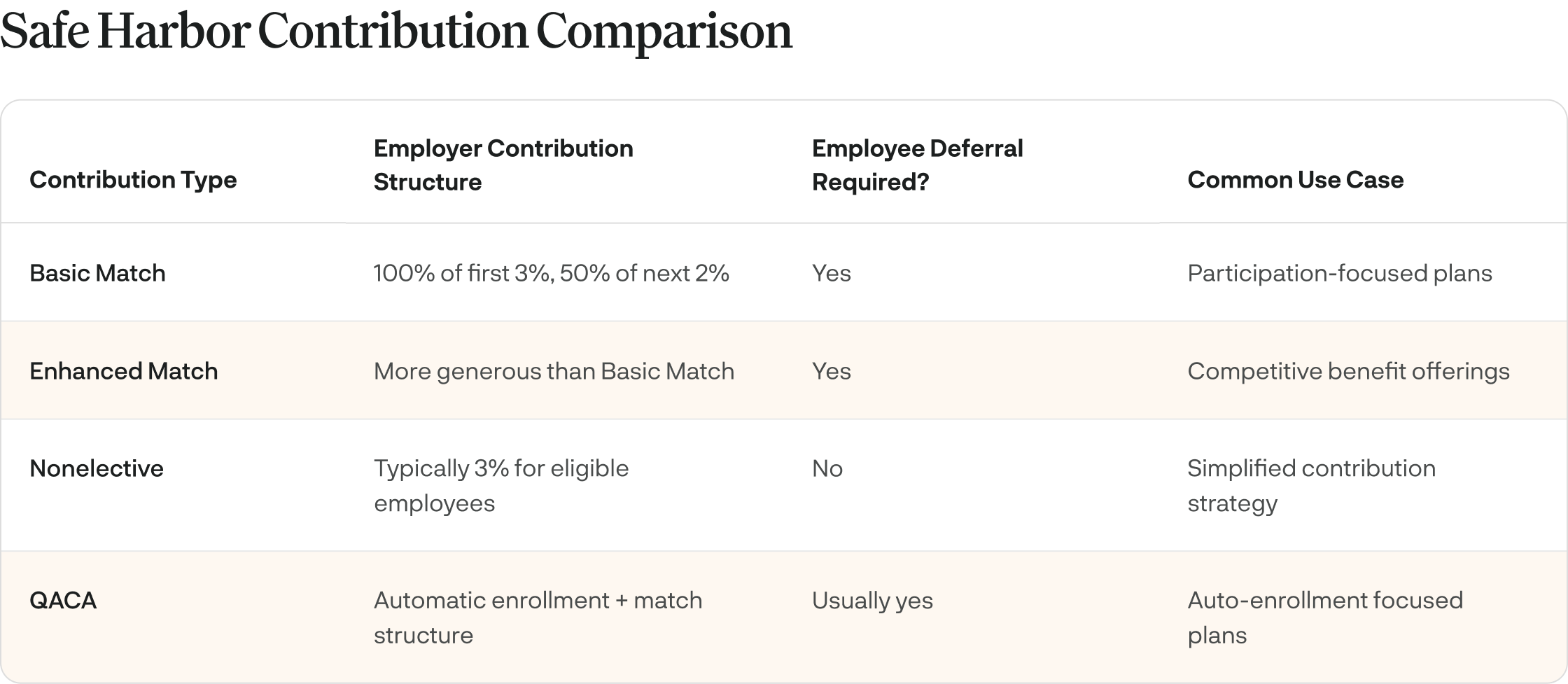

Types of Safe Harbor Contributions

One of the most defining features of a Safe Harbor plan (and what can become confusing) is the required employer contribution structure. Depending on their goals, workforce demographics, and retirement plan strategy, employers usually choose between matching contributions or nonelective contributions, but some other choices include:

Basic Safe Harbor Match

This type of match typically includes:

100% match on the first 3% of deferrals

50% match on the next 2% of deferrals

This guarantees a total employer match of up to 4%, encouraging employees to participate while also still benefitting employers’ budgets and plan strategies.

Enhanced Safe Harbor Match

Think of an enhanced Safe Harbor match as a more generous formula compared to the basic one. To qualify as an enhanced match, the formula must follow two IRS requirements:

Be generally more generous than the basic Safe Harbor match or go above the 4% total.

Apply to no more than 6% of an employee’s total compensation.

This enhanced option gives employers the chance to offer more competitive retirement benefits while strengthening recruitment and retention andkeeping participation simple for employees.

Safe Harbor Nonelective Contributions

A nonelective contribution is an employer-funded contribution made to every eligible employee’s 401(k), regardless of whether they are contributing their own money or not. Typically, employers contribute at least 3% of compensation, which is the requirement to automatically pass certain nondiscrimination tests.

QACA Safe Harbor Contributions

Qualified Automatic Contribution Arrangement (QACA) Safe Harbor plans combine automatic enrollment features with Safe Harbor contribution requirements. To stay eligible for a Safe Harbor status, employers must make either a matching or nonelective contribution following either a QACA match formula, or a nonelective contribution one. Unlike standard Safe Harbor contributions, QACA contributions can follow a two-year vesting schedule.

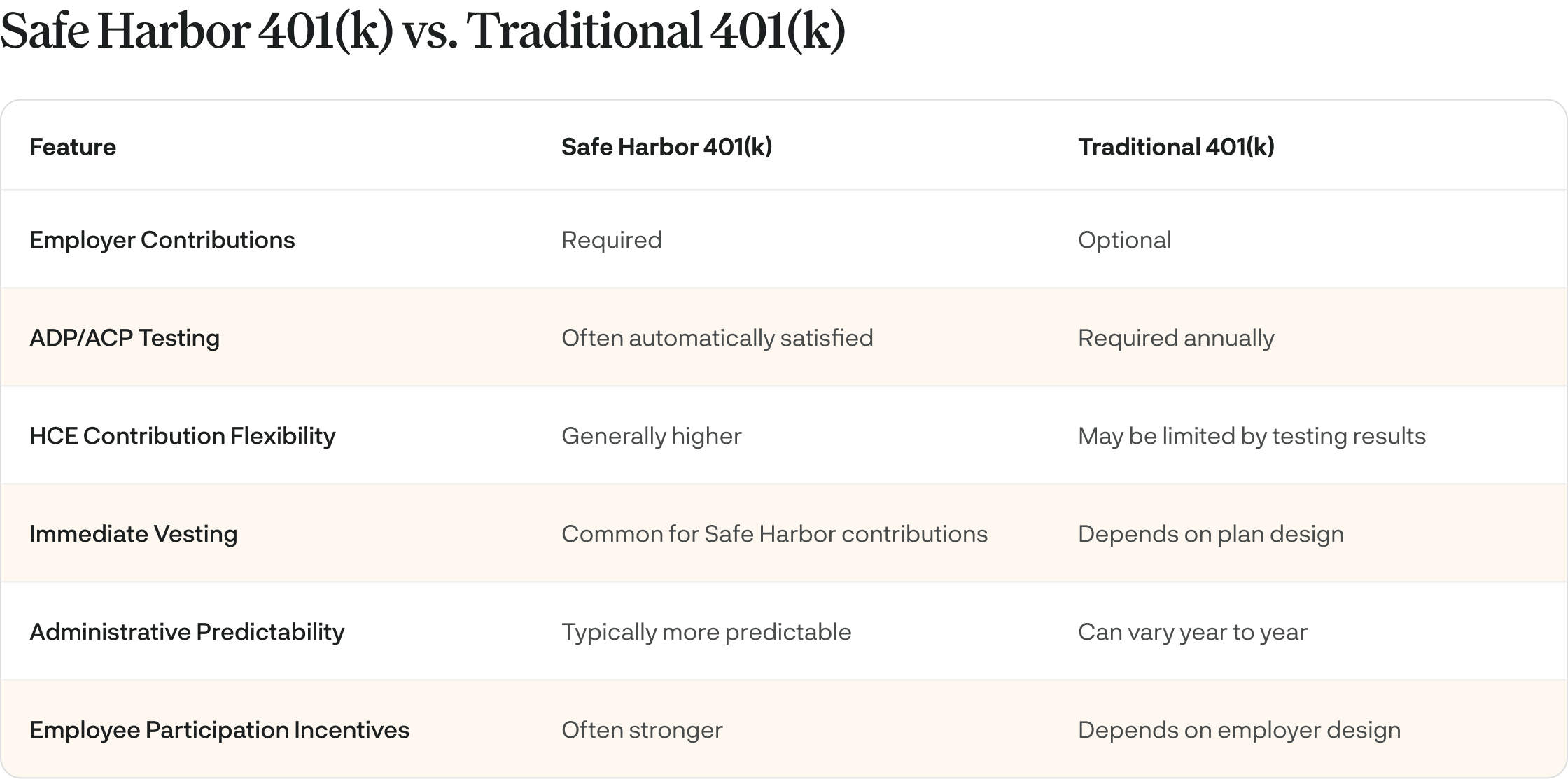

Safe Harbor vs Traditional 401(k)

One of the biggest differences is how each plan handles employer contributions and annual compliance testing. Traditional 401(k) plans may require annual nondiscrimination testing to ensure retirement benefits are properly distributed, and don’t favor highly compensated employees. On the other side, Safe Harbor plans are designed to help employers automatically satisfy testing requirements through employer contributions, potentially saving them more money and time in the long haul.

While every business has different retirement goals, Safe Harbor plans offer several advantages for employers and employees alike.

For Employers:

Simplified compliance

Greater contribution opportunities

Predictable plan costs

Competitive employee benefits

For Employees:

Employer contributions

Immediate vesting

Increased participation and satisfaction

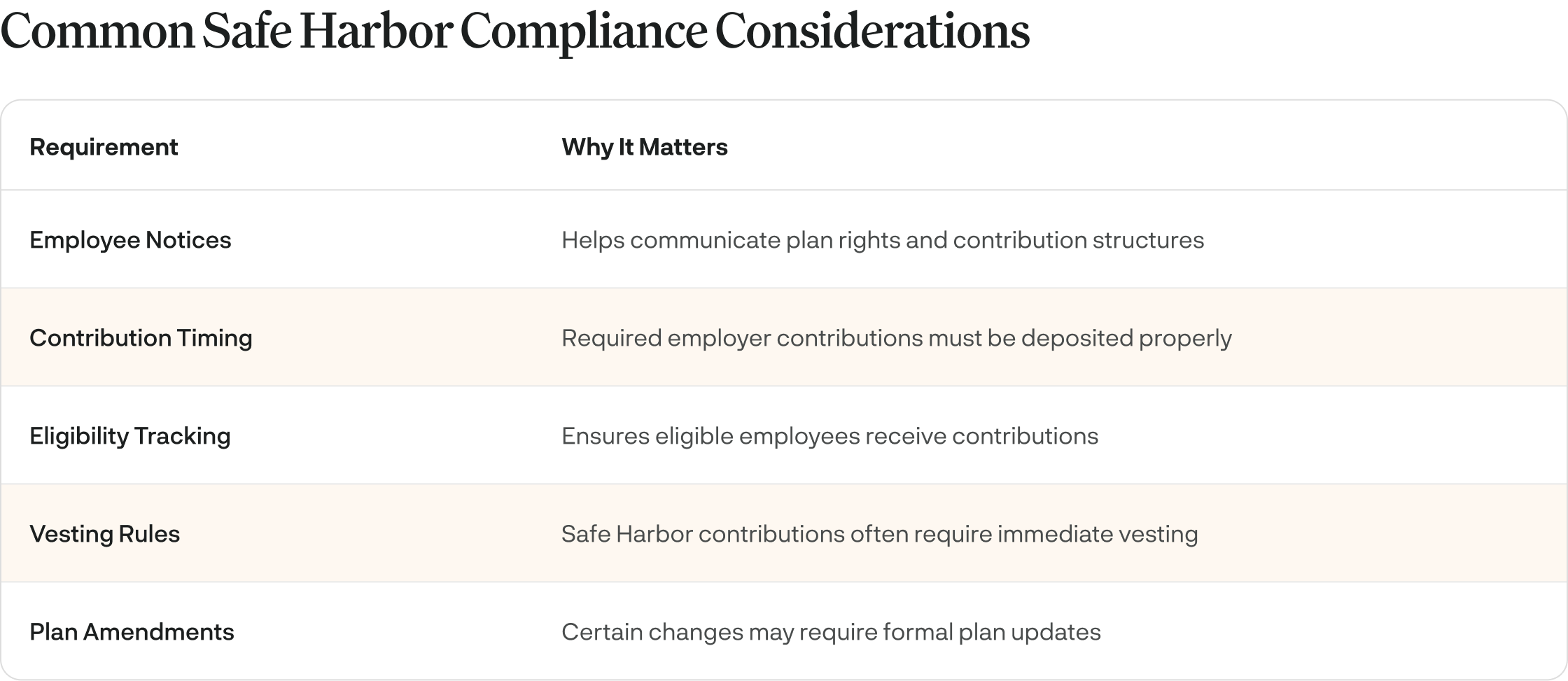

Compliance, Deadlines, and Rules

Although Safe Harbor plans can automatically satisfy testing requirements, there are still important IRS and administration rules employers must follow. These may include:

annual employee notices

contribution timing requirements

eligibility tracking

vesting requirements

payroll coordination

plan documentation updates

Safe Harbor plans can also follow different setup and amendment deadlines depending on the contribution type chosen. For example, depending on the contribution type, a Safe Harbor 401(k) may have deadlines that follow SECURE 2.0 standards, or follow traditional expectations. Plan providers, payroll partners, TPAs, and advisors play a key role in keeping these requirements on track.

Before jumping into a Safe Harbor plan, it’s important for employers to keep in mind how the SECURE 2.0 affects this type of 401(k). Specifically, there are changes that can impact how employers evaluate Safe Harbor plan design strategies.

Recent legislation now focuses more on:

automatic enrollment

retirement plan tax credits

expanded retirement access

Roth contribution flexibility

employee participation efforts

For some, a Safe Harbor 401(k) can complement these evolving strategies by providing a scalable, simplified framework.

From compliance simplicity to retirement flexibility, a Safe Harbor 401(k) can offer quite a few valuable benefits for your growing business, especially if you’re an owner looking to maximize retirement savings opportunities as soon as you can. But choosing the right plan depends on factors like workforce size and demographics, contribution goals, payroll setup, and your long-term business goals.

This is where the right retirement provider (like Ubiquity) can help simplify plan design, administration, support compliance needs, and create a retirement experience that benefits both you and your employees.

A Safe Harbor 401(k) is a type of retirement plan that allows employers to automatically bypass certain IRS-required nondiscrimination tests. In return for following certain contribution formulas, employers can benefit from simplified compliance, more employee satisfaction, and the possibility for better savings overall.

Are Safe Harbor contributions necessary?

Yes, employers must make qualifying contributions using approved Safe Harbor formulas. This ensures that their plan stays eligible, and they can take advantage of the testing and compliance benefits.

Can business owners max out contributions with a Safe Harbor plan?

Yes, because Safe Harbor plans automatically pass IRS nondiscrimination tests, employers and employees can contribute the maximum limits without worrying about refunds.

Are Safe Harbor contributions automatically vested?

Yes. In most plans, Safe Harbor contributions are immediately 100% vested. This means the funds immediately belong to employees, and they won’t have to forfeit them if they leave their current company.

Can Safe Harbor plans include profit sharing?

Yes. There are many employers that include a profit-sharing contribution in addition to the required contribution formula with their Safe Harbor 401(k). But keep in mind that because a profit-sharing contribution counts as a bonus, the plan may become subject to top-heavy requirements.

When is the deadline to set up a Safe Harbor 401(k)?

For a new Safe Harbor 401(k) plan, the deadline is October 1 for calendar year plans. This gives the plan enough time to be in effect for at least three months before year end.

Under SECURE 2.0, employers adding a Safe Harbor nonelective contribution to an existing plan have more flexibility. A 3% nonelective contribution can be added by the end of the plan year, while a 4% nonelective contribution can be added by the end of the following plan year.

recommended resource

Secure Act 2.0 Guide

This guide helps simplify upcoming changes to retirement plans due to SECURE 2.0. From tax credits to understanding compliance, Ubiquity’s got you covered!

Safe Harbor 401(k) plans have become one of the most popular retirement plan options for growing businesses, especially for owners who are looking to simplify compliance, maximize retirement contributions, and offer competitive employee benefits.

Below, you can expect to learn:

what a Safe Harbor 401(k) is

how Safe Harbor contributions work

the different Safe Harbor plan types

compliance and testing considerations

deadlines and rules employers should know

What is a Safe Harbor 401(k):

Safe Harbor 401(k) plans are designed to encourage more employee participation while helping employers satisfy specific IRS compliance requirements without extra work, especially when it comes to highly compensated employees.

With a traditional 401(k), annual nondiscrimination testing measures whether retirement benefits are fairly proportioned between highly compensated and non-highly compensated employees. If a plan fails testing, employers may need to:

issue corrective refunds

make additional employer contributions

adjust plan administration

A Safe Harbor plan reduces this risk by requiring employers to make approved contributions on behalf of employees. As long as employers follow a Safe Harbor’s rules, they can benefit from:

At first look, a Safe Harbor 401(k) can seem like a traditional plan. Employees contribute to a Safe Harbor through payroll deferral, like they would with a traditional 401(k). But the difference is that employers are required to make qualifying contributions on behalf of eligible employees using an approved Safe Harbor formula, which a plan provider can help create.

There are a few requirements to these contributions, including that they may be:

matching contributions tied to employee deferrals

nonelective contributions made regardless of participation

In return, employers can avoid certain annual testing requirements that they wouldn’t be able to get out of with a traditional 401(k).

Types of Safe Harbor Contributions

One of the most defining features of a Safe Harbor plan (and what can become confusing) is the required employer contribution structure. Depending on their goals, workforce demographics, and retirement plan strategy, employers usually choose between matching contributions or nonelective contributions, but some other choices include:

Basic Safe Harbor Match

This type of match typically includes:

100% match on the first 3% of deferrals

50% match on the next 2% of deferrals

This guarantees a total employer match of up to 4%, encouraging employees to participate while also still benefitting employers’ budgets and plan strategies.

Enhanced Safe Harbor Match

Think of an enhanced Safe Harbor match as a more generous formula compared to the basic one. To qualify as an enhanced match, the formula must follow two IRS requirements:

Be generally more generous than the basic Safe Harbor match or go above the 4% total.

Apply to no more than 6% of an employee’s total compensation.

This enhanced option gives employers the chance to offer more competitive retirement benefits while strengthening recruitment and retention andkeeping participation simple for employees.

Safe Harbor Nonelective Contributions

A nonelective contribution is an employer-funded contribution made to every eligible employee’s 401(k), regardless of whether they are contributing their own money or not. Typically, employers contribute at least 3% of compensation, which is the requirement to automatically pass certain nondiscrimination tests.

QACA Safe Harbor Contributions

Qualified Automatic Contribution Arrangement (QACA) Safe Harbor plans combine automatic enrollment features with Safe Harbor contribution requirements. To stay eligible for a Safe Harbor status, employers must make either a matching or nonelective contribution following either a QACA match formula, or a nonelective contribution one. Unlike standard Safe Harbor contributions, QACA contributions can follow a two-year vesting schedule.

Safe Harbor vs Traditional 401(k)

One of the biggest differences is how each plan handles employer contributions and annual compliance testing. Traditional 401(k) plans may require annual nondiscrimination testing to ensure retirement benefits are properly distributed, and don’t favor highly compensated employees. On the other side, Safe Harbor plans are designed to help employers automatically satisfy testing requirements through employer contributions, potentially saving them more money and time in the long haul.

While every business has different retirement goals, Safe Harbor plans offer several advantages for employers and employees alike.

For Employers:

Simplified compliance

Greater contribution opportunities

Predictable plan costs

Competitive employee benefits

For Employees:

Employer contributions

Immediate vesting

Increased participation and satisfaction

Compliance, Deadlines, and Rules

Although Safe Harbor plans can automatically satisfy testing requirements, there are still important IRS and administration rules employers must follow. These may include:

annual employee notices

contribution timing requirements

eligibility tracking

vesting requirements

payroll coordination

plan documentation updates

Safe Harbor plans can also follow different setup and amendment deadlines depending on the contribution type chosen. For example, depending on the contribution type, a Safe Harbor 401(k) may have deadlines that follow SECURE 2.0 standards, or follow traditional expectations. Plan providers, payroll partners, TPAs, and advisors play a key role in keeping these requirements on track.

Before jumping into a Safe Harbor plan, it’s important for employers to keep in mind how the SECURE 2.0 affects this type of 401(k). Specifically, there are changes that can impact how employers evaluate Safe Harbor plan design strategies.

Recent legislation now focuses more on:

automatic enrollment

retirement plan tax credits

expanded retirement access

Roth contribution flexibility

employee participation efforts

For some, a Safe Harbor 401(k) can complement these evolving strategies by providing a scalable, simplified framework.

From compliance simplicity to retirement flexibility, a Safe Harbor 401(k) can offer quite a few valuable benefits for your growing business, especially if you’re an owner looking to maximize retirement savings opportunities as soon as you can. But choosing the right plan depends on factors like workforce size and demographics, contribution goals, payroll setup, and your long-term business goals.

This is where the right retirement provider (like Ubiquity) can help simplify plan design, administration, support compliance needs, and create a retirement experience that benefits both you and your employees.

A Safe Harbor 401(k) is a type of retirement plan that allows employers to automatically bypass certain IRS-required nondiscrimination tests. In return for following certain contribution formulas, employers can benefit from simplified compliance, more employee satisfaction, and the possibility for better savings overall.

Are Safe Harbor contributions necessary?

Yes, employers must make qualifying contributions using approved Safe Harbor formulas. This ensures that their plan stays eligible, and they can take advantage of the testing and compliance benefits.

Can business owners max out contributions with a Safe Harbor plan?

Yes, because Safe Harbor plans automatically pass IRS nondiscrimination tests, employers and employees can contribute the maximum limits without worrying about refunds.

Are Safe Harbor contributions automatically vested?

Yes. In most plans, Safe Harbor contributions are immediately 100% vested. This means the funds immediately belong to employees, and they won’t have to forfeit them if they leave their current company.

Can Safe Harbor plans include profit sharing?

Yes. There are many employers that include a profit-sharing contribution in addition to the required contribution formula with their Safe Harbor 401(k). But keep in mind that because a profit-sharing contribution counts as a bonus, the plan may become subject to top-heavy requirements.

When is the deadline to set up a Safe Harbor 401(k)?

For a new Safe Harbor 401(k) plan, the deadline is October 1 for calendar year plans. This gives the plan enough time to be in effect for at least three months before year end.

Under SECURE 2.0, employers adding a Safe Harbor nonelective contribution to an existing plan have more flexibility. A 3% nonelective contribution can be added by the end of the plan year, while a 4% nonelective contribution can be added by the end of the following plan year.

Watch on-demand

Enter a few of your details below to view the webinar

Thank you!

Your submission has been received! Now you can watch the webinar on-demand by clicking the button below.

Safe Harbor 401(k) plans have become one of the most popular retirement plan options for growing businesses, especially for owners who are looking to simplify compliance, maximize retirement contributions, and offer competitive employee benefits.

Below, you can expect to learn:

what a Safe Harbor 401(k) is

how Safe Harbor contributions work

the different Safe Harbor plan types

compliance and testing considerations

deadlines and rules employers should know

What is a Safe Harbor 401(k):

Safe Harbor 401(k) plans are designed to encourage more employee participation while helping employers satisfy specific IRS compliance requirements without extra work, especially when it comes to highly compensated employees.

With a traditional 401(k), annual nondiscrimination testing measures whether retirement benefits are fairly proportioned between highly compensated and non-highly compensated employees. If a plan fails testing, employers may need to:

issue corrective refunds

make additional employer contributions

adjust plan administration

A Safe Harbor plan reduces this risk by requiring employers to make approved contributions on behalf of employees. As long as employers follow a Safe Harbor’s rules, they can benefit from:

At first look, a Safe Harbor 401(k) can seem like a traditional plan. Employees contribute to a Safe Harbor through payroll deferral, like they would with a traditional 401(k). But the difference is that employers are required to make qualifying contributions on behalf of eligible employees using an approved Safe Harbor formula, which a plan provider can help create.

There are a few requirements to these contributions, including that they may be:

matching contributions tied to employee deferrals

nonelective contributions made regardless of participation

In return, employers can avoid certain annual testing requirements that they wouldn’t be able to get out of with a traditional 401(k).

Types of Safe Harbor Contributions

One of the most defining features of a Safe Harbor plan (and what can become confusing) is the required employer contribution structure. Depending on their goals, workforce demographics, and retirement plan strategy, employers usually choose between matching contributions or nonelective contributions, but some other choices include:

Basic Safe Harbor Match

This type of match typically includes:

100% match on the first 3% of deferrals

50% match on the next 2% of deferrals

This guarantees a total employer match of up to 4%, encouraging employees to participate while also still benefitting employers’ budgets and plan strategies.

Enhanced Safe Harbor Match

Think of an enhanced Safe Harbor match as a more generous formula compared to the basic one. To qualify as an enhanced match, the formula must follow two IRS requirements:

Be generally more generous than the basic Safe Harbor match or go above the 4% total.

Apply to no more than 6% of an employee’s total compensation.

This enhanced option gives employers the chance to offer more competitive retirement benefits while strengthening recruitment and retention andkeeping participation simple for employees.

Safe Harbor Nonelective Contributions

A nonelective contribution is an employer-funded contribution made to every eligible employee’s 401(k), regardless of whether they are contributing their own money or not. Typically, employers contribute at least 3% of compensation, which is the requirement to automatically pass certain nondiscrimination tests.

QACA Safe Harbor Contributions

Qualified Automatic Contribution Arrangement (QACA) Safe Harbor plans combine automatic enrollment features with Safe Harbor contribution requirements. To stay eligible for a Safe Harbor status, employers must make either a matching or nonelective contribution following either a QACA match formula, or a nonelective contribution one. Unlike standard Safe Harbor contributions, QACA contributions can follow a two-year vesting schedule.

Safe Harbor vs Traditional 401(k)

One of the biggest differences is how each plan handles employer contributions and annual compliance testing. Traditional 401(k) plans may require annual nondiscrimination testing to ensure retirement benefits are properly distributed, and don’t favor highly compensated employees. On the other side, Safe Harbor plans are designed to help employers automatically satisfy testing requirements through employer contributions, potentially saving them more money and time in the long haul.

While every business has different retirement goals, Safe Harbor plans offer several advantages for employers and employees alike.

For Employers:

Simplified compliance

Greater contribution opportunities

Predictable plan costs

Competitive employee benefits

For Employees:

Employer contributions

Immediate vesting

Increased participation and satisfaction

Compliance, Deadlines, and Rules

Although Safe Harbor plans can automatically satisfy testing requirements, there are still important IRS and administration rules employers must follow. These may include:

annual employee notices

contribution timing requirements

eligibility tracking

vesting requirements

payroll coordination

plan documentation updates

Safe Harbor plans can also follow different setup and amendment deadlines depending on the contribution type chosen. For example, depending on the contribution type, a Safe Harbor 401(k) may have deadlines that follow SECURE 2.0 standards, or follow traditional expectations. Plan providers, payroll partners, TPAs, and advisors play a key role in keeping these requirements on track.

Before jumping into a Safe Harbor plan, it’s important for employers to keep in mind how the SECURE 2.0 affects this type of 401(k). Specifically, there are changes that can impact how employers evaluate Safe Harbor plan design strategies.

Recent legislation now focuses more on:

automatic enrollment

retirement plan tax credits

expanded retirement access

Roth contribution flexibility

employee participation efforts

For some, a Safe Harbor 401(k) can complement these evolving strategies by providing a scalable, simplified framework.

From compliance simplicity to retirement flexibility, a Safe Harbor 401(k) can offer quite a few valuable benefits for your growing business, especially if you’re an owner looking to maximize retirement savings opportunities as soon as you can. But choosing the right plan depends on factors like workforce size and demographics, contribution goals, payroll setup, and your long-term business goals.

This is where the right retirement provider (like Ubiquity) can help simplify plan design, administration, support compliance needs, and create a retirement experience that benefits both you and your employees.

A Safe Harbor 401(k) is a type of retirement plan that allows employers to automatically bypass certain IRS-required nondiscrimination tests. In return for following certain contribution formulas, employers can benefit from simplified compliance, more employee satisfaction, and the possibility for better savings overall.

Are Safe Harbor contributions necessary?

Yes, employers must make qualifying contributions using approved Safe Harbor formulas. This ensures that their plan stays eligible, and they can take advantage of the testing and compliance benefits.

Can business owners max out contributions with a Safe Harbor plan?

Yes, because Safe Harbor plans automatically pass IRS nondiscrimination tests, employers and employees can contribute the maximum limits without worrying about refunds.

Are Safe Harbor contributions automatically vested?

Yes. In most plans, Safe Harbor contributions are immediately 100% vested. This means the funds immediately belong to employees, and they won’t have to forfeit them if they leave their current company.

Can Safe Harbor plans include profit sharing?

Yes. There are many employers that include a profit-sharing contribution in addition to the required contribution formula with their Safe Harbor 401(k). But keep in mind that because a profit-sharing contribution counts as a bonus, the plan may become subject to top-heavy requirements.

When is the deadline to set up a Safe Harbor 401(k)?

For a new Safe Harbor 401(k) plan, the deadline is October 1 for calendar year plans. This gives the plan enough time to be in effect for at least three months before year end.

Under SECURE 2.0, employers adding a Safe Harbor nonelective contribution to an existing plan have more flexibility. A 3% nonelective contribution can be added by the end of the plan year, while a 4% nonelective contribution can be added by the end of the following plan year.

Get your guide

Enter your details below to download your free PDF now

Thank you!

Your submission has been received! Now you can download the guide by clicking the button below.