Safe Harbor 401(k) plans now make up over half of new small business retirement plans, driven by automatic IRS test passage, immediate vesting, and SECURE 2.0 tax credits.

Eligible small businesses can claim up to $16,500 in combined SECURE 2.0 tax credits over the first three years for adopting a Safe Harbor plan with automatic enrollment.

The most common Safe Harbor formulas are basic match, enhanced match, and 3% nonelective contributions, accounting for roughly 79% of plans, while QACA hybrid structures continue to grow.

As the retirement landscape continues to change, one thing that is holding its ground is Safe Harbor 401(k) plans. Thanks to new incentives and features, the ability to bypass IRS compliance tests, and growing concerns around economic changes and state mandates, more businesses are turning to Safe Harbor plans as a future-proof, safer way to offer competitive retirement benefits.

At Ubiquity, over 53% of our plans include a Safe Harbor provision, and that percentage is expected to grow even more as this plan design continues to resonate with employers that need compliance flexibility that doesn’t sacrifice savings possibilities.

Whether you already have a plan and are thinking of upgrading or are starting from scratch, we'll help you understand how a Safe Harbor 401(k) can help you and become a straightforward asset that enhances your business stack.

Why Safe Harbor Plans are Popular in 2026

At first look, a Safe Harbor 401(k) may seem like just a compliance shortcut, but they're much more than that. They're also a strategic tool that can enhance business profitability and employee engagement. Here's why more employers are going the Safe Harbor route:

Bypass annual nondiscrimination testing

A Safe Harbor plan automatically satisfies certain compliance tests, which means businesses no longer need to spend time and money figuring out how to stay compliant and solve various issues.

Immediate vesting and maximum contributions

HCEs are allowed to contribute the full IRS limit—$24,500 in 2026—without being restricted or triggering issues for noncompliance. Additionally, employer contributions are immediately vested, boosting the savings all around.

SECURE 2.0 tax credits

On top of the operational savings a Safe Harbor provides, businesses may also qualify for up to $16,500 in tax credits thanks to SECURE 2.0. This can help offset setup costs and more for the first three years.

Simplified compliance with automatic enrollment

To take the weight off compliance even more, businesses have access to features like Qualified Automatic Contribution Arrangements (QACAs), making plans easier to maintain and ensuring employee participation.

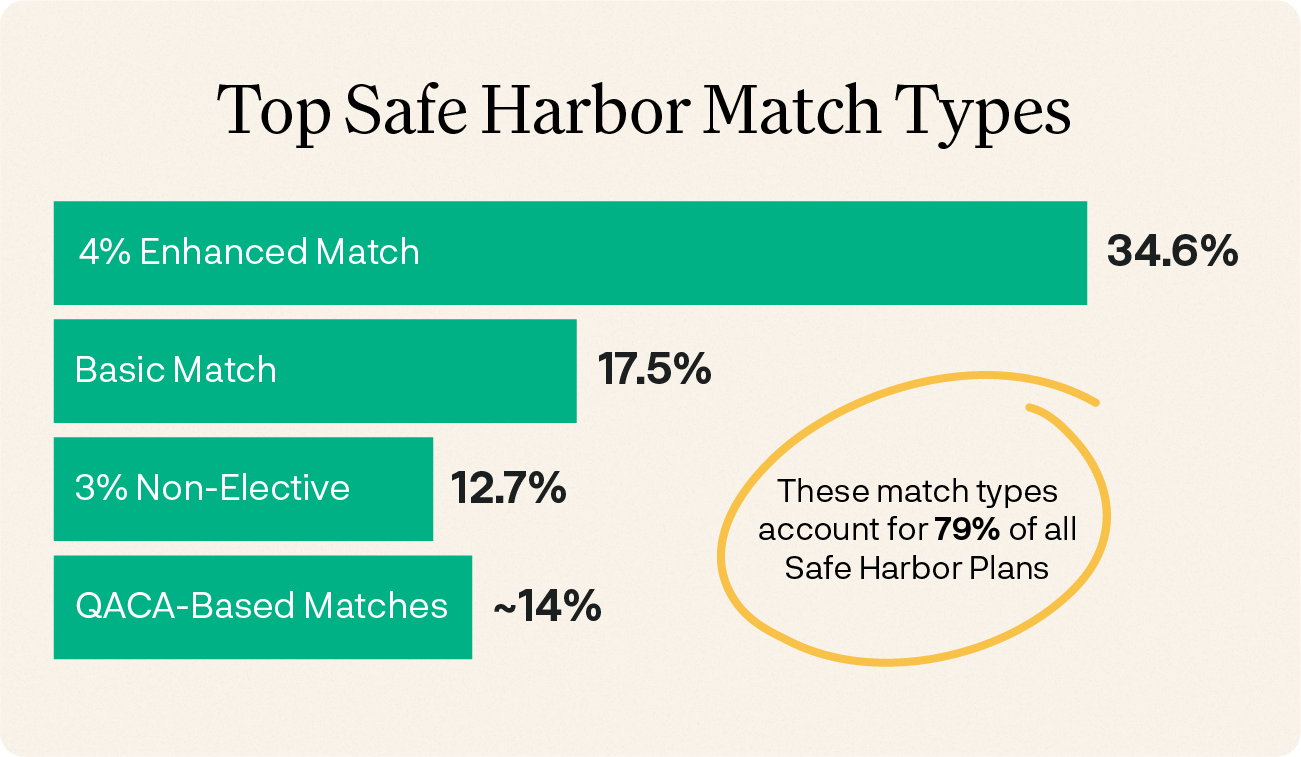

Top Safe Harbor Match Types

While the compliance benefits are the same across the board, match formulas vary with Safe Harbor plans. Here are the most common types in 2026:

It’s important to note that these percentages account for around 79% of all Safe Harbor plans. The other 21% utilize alternative formulas, like hybrid QACA structures, proving how flexible and customizable these plans truly are.

Safe Harbor Adoption by Industry

Safe Harbor 401(k) plans are used widely by many different industries. The top industries by plan count in 2026 are:

Additionally, industries with high competition for skilled labor (tech, finance, etc.) tend to leverage more robust match formulas while those that might have higher turnover rates (like construction) look for more cost predictability and simplicity.

Which States are Utilizing Safe Harbor Plans the Most?

Safe Harbor adoption is expanding coast to coast. The top states that have active plans include: Arizona, California, Colorado, Florida, Georgia, Illinois, Michigan, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Texas, Virginia, and Washington.

Many of these states, including California, Virginia, and Colorado, have active state mandates. This means that businesses are looking for more robust plan alternatives instead of just going with their state-run plan, and that’s where Safe Harbor 401(k)s come in handy.

A Safe Harbor plan ensures:

Employers have more control over their benefits

Tax credits actually get leveraged

Employees can benefit from higher contributions and tax savings

How Does the SECURE 2.0 Act Impact a Safe Harbor Plan?

With the progress SECURE 2.0 has made in recent years, it’s truly reshaping how Safe Harbor plans are set up and administered. Thanks to it, employers now have more incentives than ever.

Automatic enrollment for new plans

In 2025, most new 401(k) plans must include automatic enrollment, which is expected to drive QACAs and help employees stay engaged with their workplace’s plan earlier (unless they opt out).

Flexible nonelective deadlines

A 3% or 4% nonelective contribution can now be adopted by December 31 of the current plan year, which is a much longer deadline than what was previously allowed.

Employer Roth match contributions

Employees have more post-tax savings options as SECURE 2.0 allows employer matches to be made on a Roth basis.

Roth catch-up requirement for high earners

Beginning in 2026, employees who earned more than $150,000 in the prior year must make their age-based catch-up contributions as Roth (after-tax) deferrals. Plans that don't offer Roth contributions will need to add this option to allow affected employees to continue making catch-up contributions.

Fewer notice requirements

If you use a 3% or 4% nonelective contribution, you won’t have to distribute annual Safe Harbor notices any longer, savings you even more time on administration.

What Should Employers Do Now?

Here’s how employers can get ahead of Safe Harbor strategizing:

Evaluate your plan design before 12/31 – Depending on your workforce needs, it’s important to explore whether a Basic, Enhanced, or QACA Safe Harbor formula will work best for your business.

Ensure you’ll meet deadlines – New plans with Safe Harbor matching must be established by October 1, 20265. If you’re adding a Safe Harbor provision to an existing plan, you must do this by November 17, 2026. 3% and 4% nonelective contributions are available until December 31, 2026.

Upgrade your plan design – Basic, Enhanced, and QACA plan formulas can impact your business in different ways and unlock various benefits. Explore what fits your business best and make the change when you’re ready!

Take advantage of tax credits – Like we mentioned earlier, employers may receive up to $16,500 in tax credits if they’re eligible.

Connect with your provider – Having a consultation with your plan provider (like Ubiquity) is essential. They can help you strategize and choose a Safe Harbor approach that meets your goals.

Next Steps on Your Safe Harbor Journey

With pressures from state retirement mandates and economic volatility, 2026 is a pivotal year for Safe Harbor 401(k)s. These plans can help businesses stay compliant and simplify processes while optimizing tax benefits and savings.

Ubiquity is one provider that has redefined Safe Harbor plans (and other major retirement offerings) with benefits like customized plan design, educational tools and guides, and flat-fee pricing (no AUM fees here). With our approach, it’s truly easy for employers to stay compliant and competitive, and for their employees to meet their savings goals.

Frequently Asked Questions

What is a Safe Harbor 401(k) plan and how does it work?

Think of a Safe Harbor plan as an alternative to a traditional 401(k) that allows you to bypass certain IRS compliance tests by making required contributions to your employees’ accounts.

What are the most popular Safe Harbor match types?

In 2026, the most common match type is 4% Enhanced Match, with Basic Match and 3% Enhanced Match following. QACA-based formulas are also gaining traction due to their advantages like automatic enrollment features and tax credit eligibility.

How is a Safe Harbor plan impacted by SECURE 2.0?

With SECURE 2.0, businesses can maximize their Safe Harbor 401(k) savings with tax credits. If they qualify, they may be able to get up to $16,500 in tax credits. Additionally, SECURE allows employers to retroactively adopt a 3% nonelective plan, which is especially useful for those who find out last minute that their current plan may not pass nondiscrimination tests.

What are the deadlines to adopt a Safe Harbor plan?

To ensure you’re able to have a Safe Harbor 401(k) with a 10/1/2026 effective date, you must have your paperwork submitted by September 15, 2026. Amendments can be made until November 17, and 3% nonelective plans can be adopted until December 31.

Which states are affected by state mandates?

California, Illinois, New Jersey, Colorado, Virginia, Oregon, Connecticut, and Maryland are among the states that have active state mandates, and their laws require employers to offer qualifying retirement plans or to enroll in their state’s plan.

recommended resource

Safe Harbor 401k Guide for Your Small Business

Here’s everything you need to know about elevating your business with a Safe Harbor 401(k) plan.

As the retirement landscape continues to change, one thing that is holding its ground is Safe Harbor 401(k) plans. Thanks to new incentives and features, the ability to bypass IRS compliance tests, and growing concerns around economic changes and state mandates, more businesses are turning to Safe Harbor plans as a future-proof, safer way to offer competitive retirement benefits.

At Ubiquity, over 53% of our plans include a Safe Harbor provision, and that percentage is expected to grow even more as this plan design continues to resonate with employers that need compliance flexibility that doesn’t sacrifice savings possibilities.

Whether you already have a plan and are thinking of upgrading or are starting from scratch, we'll help you understand how a Safe Harbor 401(k) can help you and become a straightforward asset that enhances your business stack.

Why Safe Harbor Plans are Popular in 2026

At first look, a Safe Harbor 401(k) may seem like just a compliance shortcut, but they're much more than that. They're also a strategic tool that can enhance business profitability and employee engagement. Here's why more employers are going the Safe Harbor route:

Bypass annual nondiscrimination testing

A Safe Harbor plan automatically satisfies certain compliance tests, which means businesses no longer need to spend time and money figuring out how to stay compliant and solve various issues.

Immediate vesting and maximum contributions

HCEs are allowed to contribute the full IRS limit—$24,500 in 2026—without being restricted or triggering issues for noncompliance. Additionally, employer contributions are immediately vested, boosting the savings all around.

SECURE 2.0 tax credits

On top of the operational savings a Safe Harbor provides, businesses may also qualify for up to $16,500 in tax credits thanks to SECURE 2.0. This can help offset setup costs and more for the first three years.

Simplified compliance with automatic enrollment

To take the weight off compliance even more, businesses have access to features like Qualified Automatic Contribution Arrangements (QACAs), making plans easier to maintain and ensuring employee participation.

Top Safe Harbor Match Types

While the compliance benefits are the same across the board, match formulas vary with Safe Harbor plans. Here are the most common types in 2026:

It’s important to note that these percentages account for around 79% of all Safe Harbor plans. The other 21% utilize alternative formulas, like hybrid QACA structures, proving how flexible and customizable these plans truly are.

Safe Harbor Adoption by Industry

Safe Harbor 401(k) plans are used widely by many different industries. The top industries by plan count in 2026 are:

Additionally, industries with high competition for skilled labor (tech, finance, etc.) tend to leverage more robust match formulas while those that might have higher turnover rates (like construction) look for more cost predictability and simplicity.

Which States are Utilizing Safe Harbor Plans the Most?

Safe Harbor adoption is expanding coast to coast. The top states that have active plans include: Arizona, California, Colorado, Florida, Georgia, Illinois, Michigan, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Texas, Virginia, and Washington.

Many of these states, including California, Virginia, and Colorado, have active state mandates. This means that businesses are looking for more robust plan alternatives instead of just going with their state-run plan, and that’s where Safe Harbor 401(k)s come in handy.

A Safe Harbor plan ensures:

Employers have more control over their benefits

Tax credits actually get leveraged

Employees can benefit from higher contributions and tax savings

How Does the SECURE 2.0 Act Impact a Safe Harbor Plan?

With the progress SECURE 2.0 has made in recent years, it’s truly reshaping how Safe Harbor plans are set up and administered. Thanks to it, employers now have more incentives than ever.

Automatic enrollment for new plans

In 2025, most new 401(k) plans must include automatic enrollment, which is expected to drive QACAs and help employees stay engaged with their workplace’s plan earlier (unless they opt out).

Flexible nonelective deadlines

A 3% or 4% nonelective contribution can now be adopted by December 31 of the current plan year, which is a much longer deadline than what was previously allowed.

Employer Roth match contributions

Employees have more post-tax savings options as SECURE 2.0 allows employer matches to be made on a Roth basis.

Roth catch-up requirement for high earners

Beginning in 2026, employees who earned more than $150,000 in the prior year must make their age-based catch-up contributions as Roth (after-tax) deferrals. Plans that don't offer Roth contributions will need to add this option to allow affected employees to continue making catch-up contributions.

Fewer notice requirements

If you use a 3% or 4% nonelective contribution, you won’t have to distribute annual Safe Harbor notices any longer, savings you even more time on administration.

What Should Employers Do Now?

Here’s how employers can get ahead of Safe Harbor strategizing:

Evaluate your plan design before 12/31 – Depending on your workforce needs, it’s important to explore whether a Basic, Enhanced, or QACA Safe Harbor formula will work best for your business.

Ensure you’ll meet deadlines – New plans with Safe Harbor matching must be established by October 1, 20265. If you’re adding a Safe Harbor provision to an existing plan, you must do this by November 17, 2026. 3% and 4% nonelective contributions are available until December 31, 2026.

Upgrade your plan design – Basic, Enhanced, and QACA plan formulas can impact your business in different ways and unlock various benefits. Explore what fits your business best and make the change when you’re ready!

Take advantage of tax credits – Like we mentioned earlier, employers may receive up to $16,500 in tax credits if they’re eligible.

Connect with your provider – Having a consultation with your plan provider (like Ubiquity) is essential. They can help you strategize and choose a Safe Harbor approach that meets your goals.

Next Steps on Your Safe Harbor Journey

With pressures from state retirement mandates and economic volatility, 2026 is a pivotal year for Safe Harbor 401(k)s. These plans can help businesses stay compliant and simplify processes while optimizing tax benefits and savings.

Ubiquity is one provider that has redefined Safe Harbor plans (and other major retirement offerings) with benefits like customized plan design, educational tools and guides, and flat-fee pricing (no AUM fees here). With our approach, it’s truly easy for employers to stay compliant and competitive, and for their employees to meet their savings goals.

Frequently Asked Questions

What is a Safe Harbor 401(k) plan and how does it work?

Think of a Safe Harbor plan as an alternative to a traditional 401(k) that allows you to bypass certain IRS compliance tests by making required contributions to your employees’ accounts.

What are the most popular Safe Harbor match types?

In 2026, the most common match type is 4% Enhanced Match, with Basic Match and 3% Enhanced Match following. QACA-based formulas are also gaining traction due to their advantages like automatic enrollment features and tax credit eligibility.

How is a Safe Harbor plan impacted by SECURE 2.0?

With SECURE 2.0, businesses can maximize their Safe Harbor 401(k) savings with tax credits. If they qualify, they may be able to get up to $16,500 in tax credits. Additionally, SECURE allows employers to retroactively adopt a 3% nonelective plan, which is especially useful for those who find out last minute that their current plan may not pass nondiscrimination tests.

What are the deadlines to adopt a Safe Harbor plan?

To ensure you’re able to have a Safe Harbor 401(k) with a 10/1/2026 effective date, you must have your paperwork submitted by September 15, 2026. Amendments can be made until November 17, and 3% nonelective plans can be adopted until December 31.

Which states are affected by state mandates?

California, Illinois, New Jersey, Colorado, Virginia, Oregon, Connecticut, and Maryland are among the states that have active state mandates, and their laws require employers to offer qualifying retirement plans or to enroll in their state’s plan.

Watch on-demand

Enter a few of your details below to view the webinar

Thank you!

Your submission has been received! Now you can watch the webinar on-demand by clicking the button below.

As the retirement landscape continues to change, one thing that is holding its ground is Safe Harbor 401(k) plans. Thanks to new incentives and features, the ability to bypass IRS compliance tests, and growing concerns around economic changes and state mandates, more businesses are turning to Safe Harbor plans as a future-proof, safer way to offer competitive retirement benefits.

At Ubiquity, over 53% of our plans include a Safe Harbor provision, and that percentage is expected to grow even more as this plan design continues to resonate with employers that need compliance flexibility that doesn’t sacrifice savings possibilities.

Whether you already have a plan and are thinking of upgrading or are starting from scratch, we'll help you understand how a Safe Harbor 401(k) can help you and become a straightforward asset that enhances your business stack.

Why Safe Harbor Plans are Popular in 2026

At first look, a Safe Harbor 401(k) may seem like just a compliance shortcut, but they're much more than that. They're also a strategic tool that can enhance business profitability and employee engagement. Here's why more employers are going the Safe Harbor route:

Bypass annual nondiscrimination testing

A Safe Harbor plan automatically satisfies certain compliance tests, which means businesses no longer need to spend time and money figuring out how to stay compliant and solve various issues.

Immediate vesting and maximum contributions

HCEs are allowed to contribute the full IRS limit—$24,500 in 2026—without being restricted or triggering issues for noncompliance. Additionally, employer contributions are immediately vested, boosting the savings all around.

SECURE 2.0 tax credits

On top of the operational savings a Safe Harbor provides, businesses may also qualify for up to $16,500 in tax credits thanks to SECURE 2.0. This can help offset setup costs and more for the first three years.

Simplified compliance with automatic enrollment

To take the weight off compliance even more, businesses have access to features like Qualified Automatic Contribution Arrangements (QACAs), making plans easier to maintain and ensuring employee participation.

Top Safe Harbor Match Types

While the compliance benefits are the same across the board, match formulas vary with Safe Harbor plans. Here are the most common types in 2026:

It’s important to note that these percentages account for around 79% of all Safe Harbor plans. The other 21% utilize alternative formulas, like hybrid QACA structures, proving how flexible and customizable these plans truly are.

Safe Harbor Adoption by Industry

Safe Harbor 401(k) plans are used widely by many different industries. The top industries by plan count in 2026 are:

Additionally, industries with high competition for skilled labor (tech, finance, etc.) tend to leverage more robust match formulas while those that might have higher turnover rates (like construction) look for more cost predictability and simplicity.

Which States are Utilizing Safe Harbor Plans the Most?

Safe Harbor adoption is expanding coast to coast. The top states that have active plans include: Arizona, California, Colorado, Florida, Georgia, Illinois, Michigan, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Texas, Virginia, and Washington.

Many of these states, including California, Virginia, and Colorado, have active state mandates. This means that businesses are looking for more robust plan alternatives instead of just going with their state-run plan, and that’s where Safe Harbor 401(k)s come in handy.

A Safe Harbor plan ensures:

Employers have more control over their benefits

Tax credits actually get leveraged

Employees can benefit from higher contributions and tax savings

How Does the SECURE 2.0 Act Impact a Safe Harbor Plan?

With the progress SECURE 2.0 has made in recent years, it’s truly reshaping how Safe Harbor plans are set up and administered. Thanks to it, employers now have more incentives than ever.

Automatic enrollment for new plans

In 2025, most new 401(k) plans must include automatic enrollment, which is expected to drive QACAs and help employees stay engaged with their workplace’s plan earlier (unless they opt out).

Flexible nonelective deadlines

A 3% or 4% nonelective contribution can now be adopted by December 31 of the current plan year, which is a much longer deadline than what was previously allowed.

Employer Roth match contributions

Employees have more post-tax savings options as SECURE 2.0 allows employer matches to be made on a Roth basis.

Roth catch-up requirement for high earners

Beginning in 2026, employees who earned more than $150,000 in the prior year must make their age-based catch-up contributions as Roth (after-tax) deferrals. Plans that don't offer Roth contributions will need to add this option to allow affected employees to continue making catch-up contributions.

Fewer notice requirements

If you use a 3% or 4% nonelective contribution, you won’t have to distribute annual Safe Harbor notices any longer, savings you even more time on administration.

What Should Employers Do Now?

Here’s how employers can get ahead of Safe Harbor strategizing:

Evaluate your plan design before 12/31 – Depending on your workforce needs, it’s important to explore whether a Basic, Enhanced, or QACA Safe Harbor formula will work best for your business.

Ensure you’ll meet deadlines – New plans with Safe Harbor matching must be established by October 1, 20265. If you’re adding a Safe Harbor provision to an existing plan, you must do this by November 17, 2026. 3% and 4% nonelective contributions are available until December 31, 2026.

Upgrade your plan design – Basic, Enhanced, and QACA plan formulas can impact your business in different ways and unlock various benefits. Explore what fits your business best and make the change when you’re ready!

Take advantage of tax credits – Like we mentioned earlier, employers may receive up to $16,500 in tax credits if they’re eligible.

Connect with your provider – Having a consultation with your plan provider (like Ubiquity) is essential. They can help you strategize and choose a Safe Harbor approach that meets your goals.

Next Steps on Your Safe Harbor Journey

With pressures from state retirement mandates and economic volatility, 2026 is a pivotal year for Safe Harbor 401(k)s. These plans can help businesses stay compliant and simplify processes while optimizing tax benefits and savings.

Ubiquity is one provider that has redefined Safe Harbor plans (and other major retirement offerings) with benefits like customized plan design, educational tools and guides, and flat-fee pricing (no AUM fees here). With our approach, it’s truly easy for employers to stay compliant and competitive, and for their employees to meet their savings goals.

Frequently Asked Questions

What is a Safe Harbor 401(k) plan and how does it work?

Think of a Safe Harbor plan as an alternative to a traditional 401(k) that allows you to bypass certain IRS compliance tests by making required contributions to your employees’ accounts.

What are the most popular Safe Harbor match types?

In 2026, the most common match type is 4% Enhanced Match, with Basic Match and 3% Enhanced Match following. QACA-based formulas are also gaining traction due to their advantages like automatic enrollment features and tax credit eligibility.

How is a Safe Harbor plan impacted by SECURE 2.0?

With SECURE 2.0, businesses can maximize their Safe Harbor 401(k) savings with tax credits. If they qualify, they may be able to get up to $16,500 in tax credits. Additionally, SECURE allows employers to retroactively adopt a 3% nonelective plan, which is especially useful for those who find out last minute that their current plan may not pass nondiscrimination tests.

What are the deadlines to adopt a Safe Harbor plan?

To ensure you’re able to have a Safe Harbor 401(k) with a 10/1/2026 effective date, you must have your paperwork submitted by September 15, 2026. Amendments can be made until November 17, and 3% nonelective plans can be adopted until December 31.

Which states are affected by state mandates?

California, Illinois, New Jersey, Colorado, Virginia, Oregon, Connecticut, and Maryland are among the states that have active state mandates, and their laws require employers to offer qualifying retirement plans or to enroll in their state’s plan.

Get your guide

Enter your details below to download your free PDF now

Thank you!

Your submission has been received! Now you can download the guide by clicking the button below.